The series so far

Estate tax protection using single-entity holding structures

The series started with a discussion of single-entity holding structures. I brain-dumped all of the holding structures I could think of, then walked you through the analysis of which structures provided estate tax protection and which didn’t.

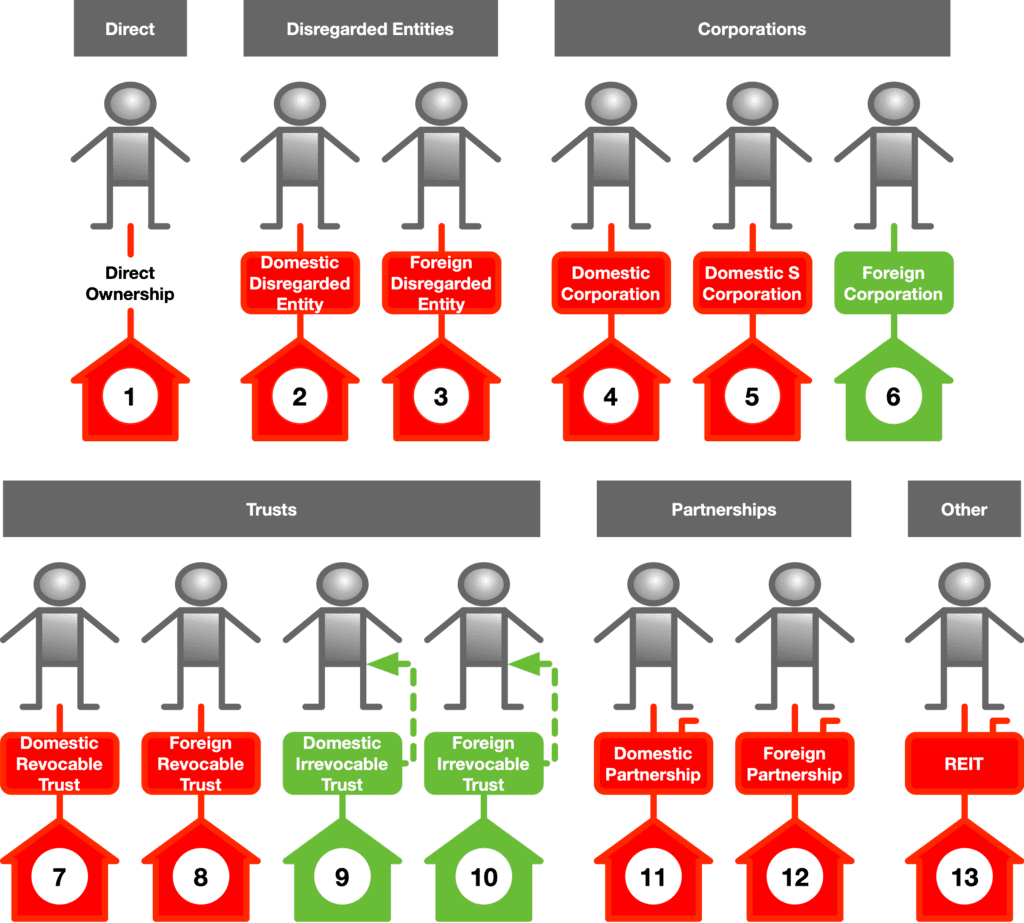

- Episode 1 – Thirteen single-level holding structures exist for possible use. (We’ll deal with multi-level holding structures later. Three are eliminated: forbidden, logically impossible, or wildly impractical.

- Episode 2 – Of the ten remaining single-level holding structures, we eliminate three because they are guaranteed to result in estate tax if the real estate owner dies.

- Episode 3 – Of the remaining seven holding structures, four have uncertain estate tax results. Some are more uncertain than others. Eliminate them: “maybe” means “no.”

- Episode 4 – Of all of the single level structures we considered, three remained. All of them guarantee estate tax protection.

Estate tax protection using multi-entity holding structures

You are here! Now I’m going to look at multi-entity holding structures. Let’s see if cleverness and complexity can provide estate tax protection as well (or better) than simplicity.

This, too, will take a few episodes to explain.

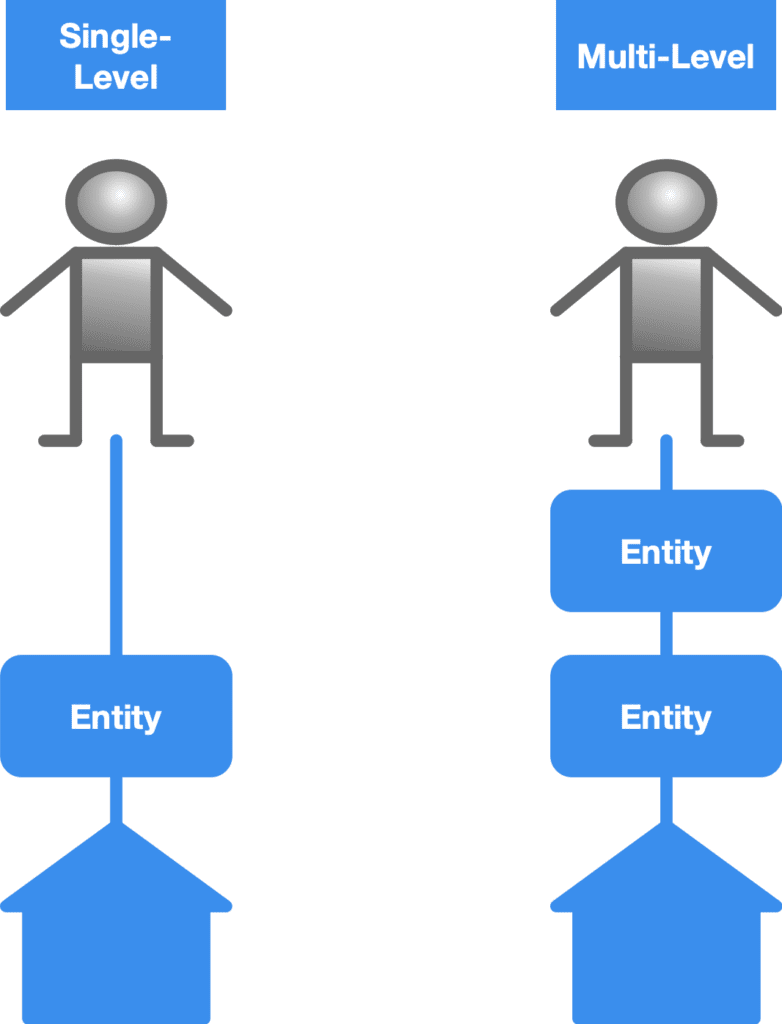

What is a multi-entity holding structure?

First, let’s define what a multi-entity holding structure is.

Think of a sandwich.

- Two pieces of bread with a slice of ham in the middle? That’s a single-entity holding structure. Investor at the top, entity in the middle, real estate on the bottom.

- Two pieces of bread with a slice of ham and a slice of cheese in the middle? That’s a multi-entity holding structure. Investor at the top, two different types of entities in the middle, real estate on the bottom.

Why use a multi-entity structure?

There are a few reasons to use a multi-entity structure. I’m only going to talk about the estate tax reasons.

Simply put: you use a multi-entity structure to add estate tax protection to a single-entity structure lacking that feature.

How a multi-entity structure adds estate tax protection

The tax principle

Remember: a nonresident-noncitizen’s gross estate consists of the decedent’s interest in property that is situated in the United States. If the gross estate has a value of $0, then estate tax will be $0, too.

How do we make sure that a nonresident-noncitizen’s gross estate is zero?

- Ensure that the nonresident-noncitizen investor does not own “an interest in property”. This is the irrevocable trust idea, remember? Make sure the person creating the trust does not have a “retained interest” (IRC §§2036-2038) and the beneficiaries do not have a “general power of appointment” (IRC §2041).

- If the nonresident-noncitizen owns an interest in property, make sure that the property is not situated in the United States. This is the foreign corporation structure, remember? Stock is located where the corporation was formed, so a foreign corporation is located outside the United States.

So remember that principle: if the gross estate is zero, the estate tax is zero.

The tools we use

We will rehabilitate broken single-entity structures by adding an irrevocable trust or a foreign corporation somewhere in the holding structure.

This will prevent estate tax if the foreign investor dies during the holding period for the real estate.

Single-entity structure candidates for enhancement with a second entity

Remember the starting diagram of all of the single-entity holding structures? Here it is again. The red structures were eliminated because they did not provide estate tax protection. The green structures, if properly executed, will provide estate tax protection.

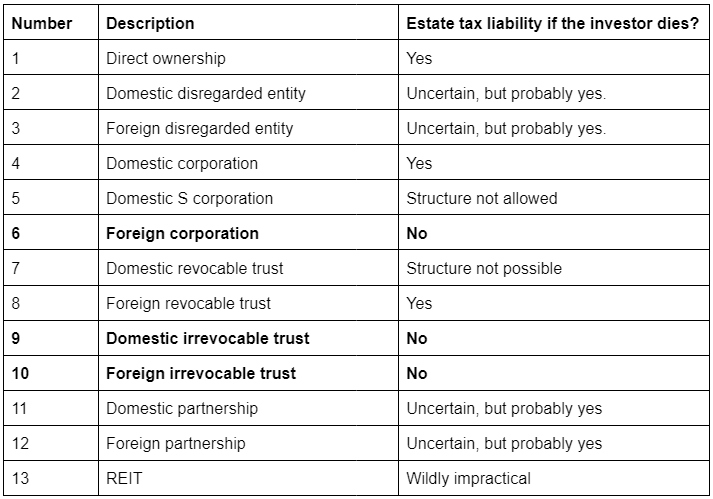

Here they are, in a glorious summary table. We will ignore the bolded structures (because they already work).

I am going to ignore holding structures 6 (foreign corporation), 9 (domestic irrevocable trust), and 10 (foreign irrevocable trust). We know these structures provide estate tax protection, so we don’t need to add more estate tax protection.

Which reminds me of a joke.

An alcoholic is walking down the street and sees a sign in the window of a bar. “All you can drink for $10.” The alcoholic walks up to the bartender and slaps down a $20. “I’ll take two.”

Direct Ownership + ???

Direct ownership + anything = single-entity structure

Structure 1 (direct ownership) plus any type of entity just means you created a single-entity structure.

We already looked at single-entity structures. We will move on.

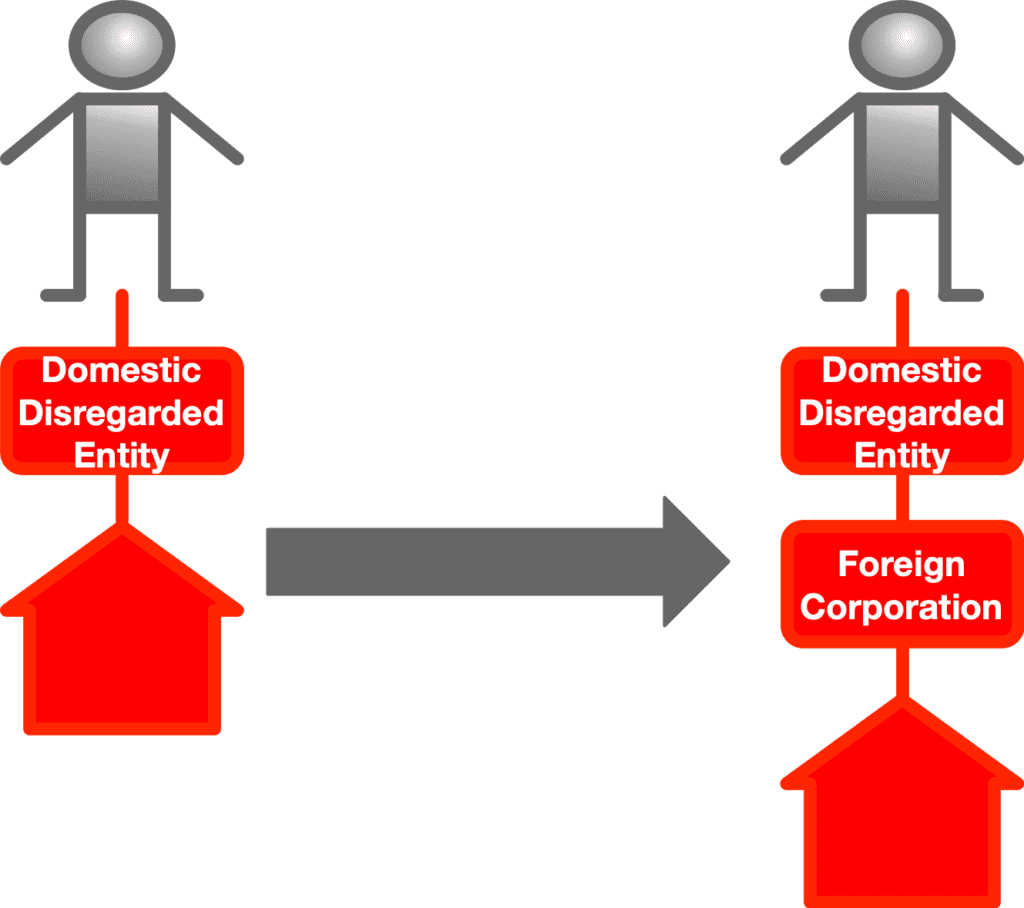

Domestic disregarded entity + foreign corporation

Structure 2 (domestic disregarded entity) as a single-entity structure failed because of uncertainty. It seems probable that estate tax will be imposed if the nonresident investor dies while owning U.S. real estate in a domestic disregarded entity, but perhaps there are arguments you could make in front of a Tax Court judge without blushing from shame and embarrassment.

Good tax planning rests on solid foundations. We rejected a single-level domestic disregarded entity holding structure because the best we could say about it is “we might have a tenuous argument in favor of no estate tax.”

Let’s see what happens when we use a domestic disregarded entity in a multi-level holding structure.

Remember that the entity that is added must either be a foreign corporation or a (domestic or foreign) irrevocable trust.

Foreign corporation underneath a domestic disregarded entity

A nonresident-noncitizen is the sole member of a domestic disregarded entity, which owns all of the stock of a foreign corporation. The foreign corporation holds title to U.S. real estate.

What does the nonresident-noncitizen’s gross estate contain? At death the nonresident-noncitizen owned a membership interest in a domestic business entity that is disregarded for U.S. tax purposes.

The pessimistic interpretation:

- The domestic disregarded entity is not disregarded for estate tax purposes because State law governs property rights and then Federal tax law dictates the tax treatment of those property rights.

- In this case, the nonresident-noncitizen owns intangible personal property (a membership interest in an LLC) situated in the United States (because it was organized under the laws of one of the 50 States or the District of Columbia.

- The membership interest in the LLC is included in the gross estate of the deceased nonresident-noncitizen.

- This is consistent with Suzanne Pierre v. Commissioner.

The optimistic interpretation:

- Disregarded means disregarded. Completely ignore the LLC for estate tax purposes.

- The nonresident-noncitizen is considered to own the shares of the foreign corporation directly.

- The gross estate of the nonresident-noncitizen would consist of stock of a foreign corporation, and that stock is situated outside the United States.

- Therefore, the stock of the foreign corporation is excluded from the gross estate.

- No estate tax is imposed.

In the real world:

- Why put up with uncertainty?

- Don’t use this structure.

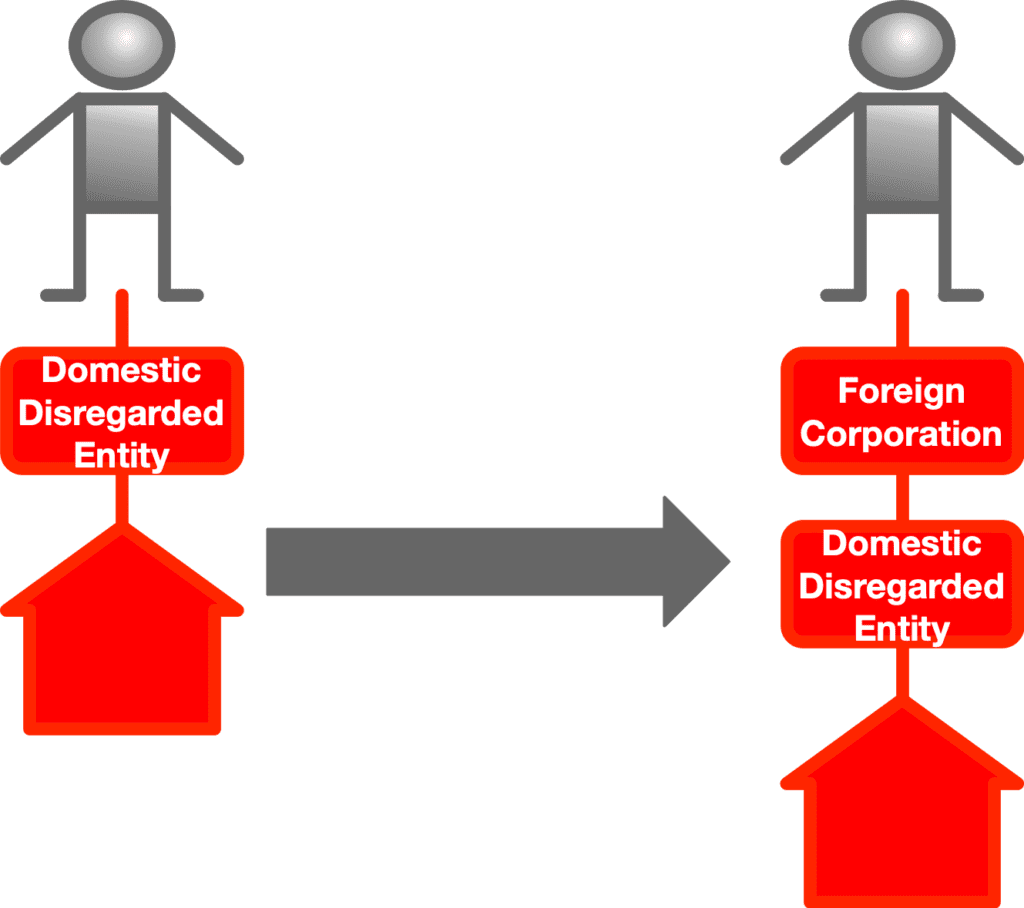

Foreign corporation above a domestic disregarded entity

This feels like an episode of Goofus and Gallant, doesn’t it?

Here’s how to do it right. The nonresident-noncitizen investor owns all of the stock of a foreign corporation, and the foreign corporation owns all of the membership interests of a domestic disregarded entity. The disregarded entity holds title to U.S. real estate.

No estate tax is imposed in the event of the death of the nonresident-noncitizen.

The nonresident-noncitizen owned an interest in property at death – stock of a foreign corporation.

The stock of the foreign corporation is situated outside the United States, because the situs rules for corporate stock follows the “Where did you form that corporation? Because that’s where the stock is located” rule.

Therefore, the decedent owned an interest in property situated outside the United States – and such an interest in property is excluded from the gross estate.

Conclusion

Let’s wrap it up here for now. Here are the principles we covered:

- To prevent estate tax from being imposed when a nonresident-noncitizen dies, make sure that there is nothing in the gross estate.

- You prevent inclusion of property in the gross estate by making sure that the decedent does not have an “interest” in the property, or by making sure that the decedent has an interest in the property but the property is situated outside the United States.

- In multi-entity structures, you need either a foreign corporation (demonstrated above) or an irrevocable trust (demonstrated next time) to act as a firewall against inclusion of property in the gross estate.

- Merely having the magic entity (foreign corporation or irrevocable trust) in the multi-entity structure is not enough. The parts must be assembled in the right sequence.