Welcome to The Friday Edition. Phil here, in the Bright and Shiny Year of Our Lord 2024. We continue in the series about holding structures for nonresidents who buy U.S. real estate.

In the last episode . . .

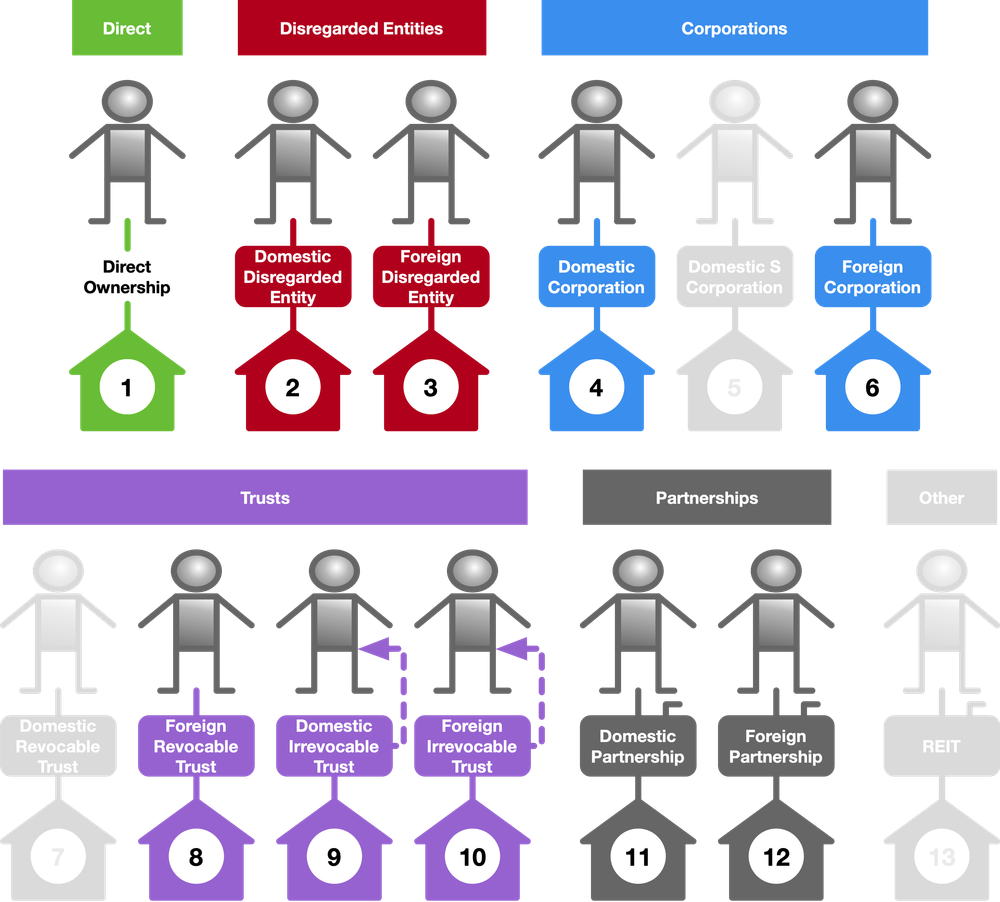

In the first episode, I showed that there are 13 types of single-level holding structures that can be used. I also showed you that three of them are prohibited, impossible, or impractical.

We cut the list from 13 to 10 candidates for holding structures.

We knocked off three choices last time (shown in light gray on the illustration above).

Now, the estate tax knock-out punch

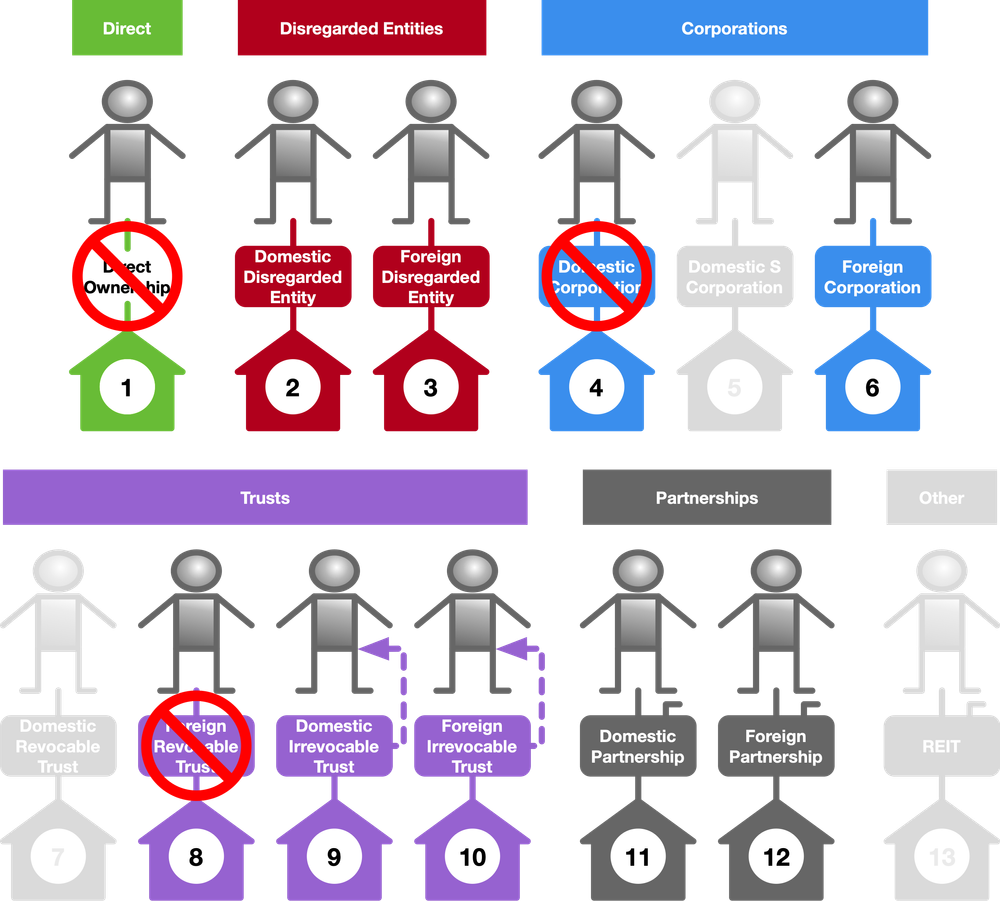

Now let’s administer the knock-out punch of estate tax to the remaining ten structure choices and see what happens.

In this episode 2, we will eliminate three more holding structures from consideration because they guarantee estate tax exposure. If the nonresident dies, estate tax must be paid.

Why estate tax is a problem for nonresidents

Estate tax is the primary tax risk for nonresidents buying U.S. real estate. Why? Because they don’t get the big unified credit. The taxable portion of the decedent’s estate starts at $60,000 of assets.

Residents and citizens have a “basic exclusion amount” (IRC §2010(c)(3)) that, adjusted for inflation, protects $13,610,000 of assets from estate tax. Rev. Proc. 2023-34, Section 3.41.

Nonresident-noncitizens, on the other hand, are allowed a unified credit of $13,000 by IRC §2102(b)(1), which translates to protecting $60,000 of assets from estate tax.

The tax issue to solve: “gross estate”

“Is there an estate tax risk with this holding structure?” is fuzzy and imprecise. Why does an estate tax risk exist?

The estate tax calculation

The estate tax calculation is simple:

- “Gross estate” minus some stuff = “taxable estate”. IRC §2106.

- “Taxable estate” multiplied by the tax rate = estate tax liability. §2101.

Internal Revenue Code

Estate tax is imposed by IRC §2101(a):

[A] tax is hereby imposed on the transfer of the taxable estate (determined as provided in section 2106) of every decedent nonresident not a citizen of the United States.

The taxable estate is the decedent’s gross estate minus some stuff. IRC §2106(a):

For purposes of the tax imposed by section 2101, the value of the taxable estate of every decedent nonresident not a citizen of the United States shall be determined by deducting from the value of that part of his gross estate which at the time of his death is situated in the United States [a laundry list follows].

The gross estate of a deceased nonresident-noncitizen is his/her “interest” in “property” “situated in the United States.”

IRC §2103 calls out the “situated in the United States” part.

For the purpose of the tax imposed by section 2101, the value of the gross estate of every decedent nonresident not a citizen of the United States shall be that part of his gross estate (determined as provided in section 2031) which at the time of his death is situated in the United States.

The “interest” in “property” part is found in the basic definition of “gross estate” at IRC §2033:

The value of the gross estate shall include the value of all property to the extent of the interest therein of the decedent at the time of his death.

If the nonresident-noncitizen’s “gross estate” has nothing in it, then estate tax must necessarily be zero.

Since three elements are required for inclusion of an asset in the gross estate (“interest” in “property” that is “situated in the United States”), let’s look at the holding structures that unambiguously satisfy all three elements.

Structures with estate tax guaranteed

The following structures have clear answers in the situs rules, and a nonresident decedent’s gross estate will have an asset in it worth taxing.

Direct ownership

Direct ownership of U.S. real estate will expose a nonresident-noncitizen’s heirs to estate tax liability risk.

Real estate is “property” and your name on title means you have an ownership “interest” in it. And nothing quite screams “situated in the United States” as some dirt located within the borders of the US and A with a building on it.

Domestic corporation

Stock in a corporation is considered to be “situated” in the jurisdiction of formation. IRC §2104(a):

For purposes of this subchapter shares of stock owned and held by a nonresident not a citizen of the United States shall be deemed property within the United States only if issued by a domestic corporation.

“Domestic” means the 50 States and the District of Columbia. IRC §7701(a)(4).

The three elements are satisfied:

- Corporate stock is intangible personal property.

- The nonresident-noncitizen’s ownership of the stock is an “interest” in that stock.

- Corporate stock issued by a domestic corporation is “situated in the United States.”

If the nonresident-nonresident dies while owning stock of a domestic corporation, the value of the stock owned will be included in his or her gross estate for U.S. estate tax purposes.

Foreign revocable trust

Someone who contributes assets to a trust and holds the power to revoke the trust is considered to hold a “retained interest” in the trust’s assets. IRC §2038(a)(1).

The trust asset in this case consists of U.S. real estate.

Therefore, the three elements are satisfied:

- The deceased nonresident-noncitizen has a (retained) interest in whatever assets are in the trust.

- The assets consist of U.S. real property, which is “property“

- And of course U.S. real property is tautologically situated in the United States.

Therefore, in the event of the nonresident-noncitizen’s death, the value of the U.S. real estate will be included in the gross estate for U.S. estate tax purposes.

Three structures eliminated

We have now eliminated three structures from contention.

In the next episode we will cull the remaining holding structures with estate tax risk. These have uncertain estate tax risk – the law is not clear. (We’re talking about disregarded entities and partnerships).

See you in two weeks with the next episode in this series: why your tax advisor’s “this should work” is worse than useless.

Workshop Announcement: CFC F Reorg

The Form 5471 Series this month (January 26, 2024) covers organization, liquidation, and reorganizations of CFCs. One hour of coverage means we can’t go deep.

If you don’t want to just dabble your toes in the water, let’s dive in and get all the way wet.

I’m going to do a workshop on CFC reorgs. It will be a deep dive into how (and why) a tax-free IRC §368 reorganization of a CFC works. It is drawn from real-life projects that I work on. We will talk about the theory as well as the practice, including the relevant tax forms. I’m going to use an F reorg of a CFC owned by a trust as an example (because I recently did one of these).

If you’re interested, email me and tell me you might want to attend the workshop.

No CPE credits, because the NASBA paperwork is a PITA so I will have accreditation in hand for future workshops sometime after Hell Freezes Over but it’s going to take a while). Likely it will be 2 hours (“legs should be long enough to reach the ground, but no longer”). And it will be for money. Likely $250.

Until next time

Email me! Let’s talk. I had a great chat with Phil T. and Moses M. last week. Let’s get on the phone. I love talking to people who are in the trenches, doing the work.

Phil.