This is the seventh episode of the real estate holding structure series. In this series I walk you through the thought process of a non-resident who wants to buy a home in the United States for personal or family use–not for rental.

This episode wraps up the discussion of estate tax.

- Episode 1 – Thirteen single-level holding structures exist for possible use. (We’ll deal with multi-level holding structures later. Three are eliminated: forbidden, logically impossible, or wildly impractical.

- Episode 2 – Of the ten remaining single-level holding structures, we eliminate three because they are guaranteed to result in estate tax if the real estate owner dies.

- Episode 3 – Of the remaining seven holding structures, four have uncertain estate tax results. Some are more uncertain than others. Eliminate them: “maybe” means “no.”

- Episode 4 – Of all of the single level structures we considered, three remain. All of them are guaranteed to provide estate tax protection.

- Episode 5 – We started looking at more complicated holding structures. We identified the two-tier holding structures to use, and then took a deep dive to look at how we can add estate tax protection by making a foreign corporation the sole member of a domestic disregarded intently instead of a nonresident individual.

- Episode 6 – This episode looks at adding a foreign corporations to other single-level holding structures: how it works, why it works, and pitfalls to avoid.

- [You are here] Episode 7 – Finally, let’s look at how you add an irrevocable trust to a broken holding structure to gain estate tax protection for a nonresident’s investment in U.S. real estate.

The Gross Estate

Assets owned by a dead person (“decedent” in legal terms) are called the “gross estate.” That’s what is subject to estate tax. If the decedent’s gross estate is worth $0, then there can be no estate tax.

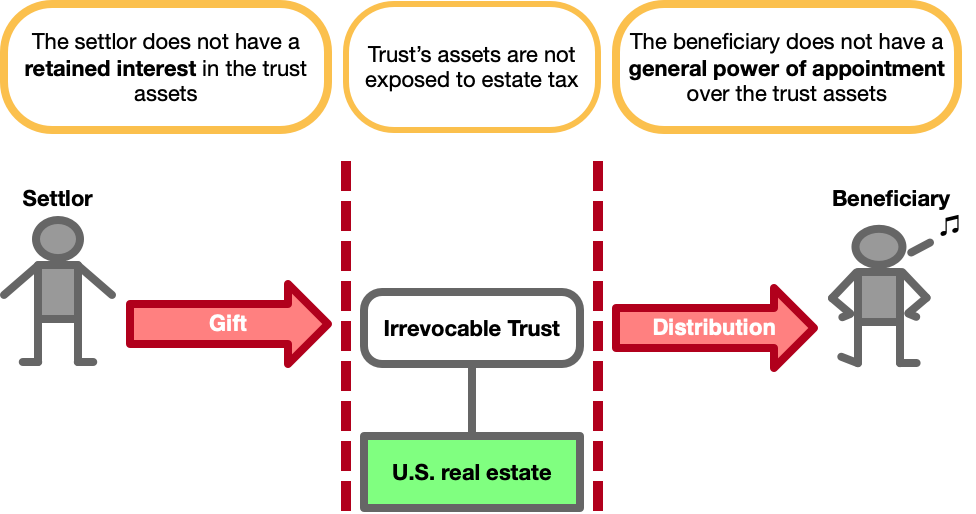

A trust has three parties:

- The Settlor (the person who creates the trust and gives assets to the trustee to hold under the terms of the trust document)

- The Trustee (the person who agrees to hold the assets and follow the instructions in the trust document)

- The Beneficiary (the person who is entitled to receive stuff from the trust).

The way a trust prevents estate tax is simple:

- The Settlor makes a completed gift to the trust and has no “retained interest” (rights defined in IRC §§2036-2038) in the trust assets. When the Settlor dies, the trust assets are not exposed to estate tax, because the Settlor does not own an “interest in property” – namely, an interest in the trust assets.

- The Beneficiary is entitled to receive distributions, typically made at the discretion of the Trustee. But the Beneficiary does not hold a general power of appointment (IRC §§2041) – the Beneficiary cannot force distribution of trust assets to himself, his creditors, or his estate. Again, this means that the Beneficiary has no ownership interest in the trust assets.

- The Trustee has technical ownership of the assets in the trust, but no economic rights to receive distributions. No ownership interest exists. The Trustee is a hired hand.

That’s how any well-configured nongrantor trust will work.

Fix a broken holding structure by adding a trust

Nonresident investors in U.S. real estate frequently hold ownership in ways that create estate tax risk. As long as they don’t die . . . everything is good.

We explored a number of holding structure methods that create estate tax problems in the previous episodes. How do you fix such a situation?

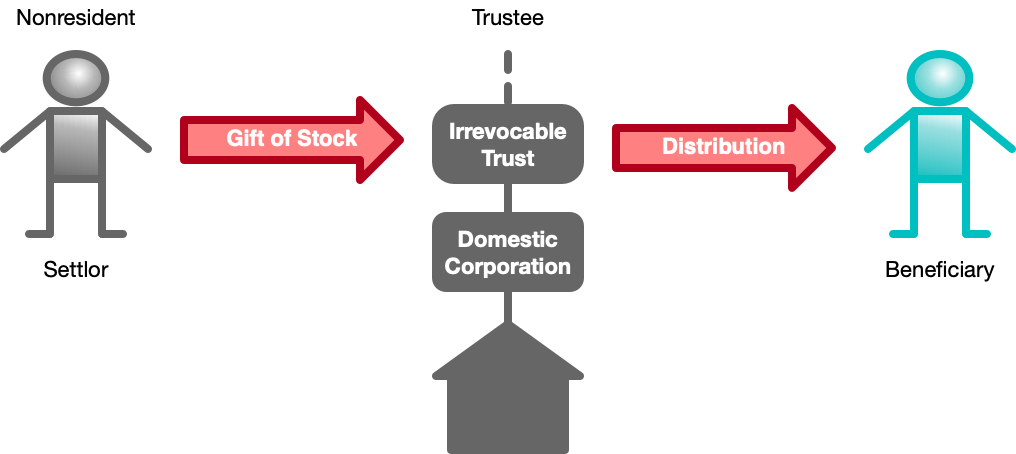

In Episode 6 I explored adding a foreign corporation to the ownership structure. Now let’s look at adding a trust – specifically, a domestic or foreign nongrantor trust – to the structure.

Use as an example a nonresident who forms a U.S. corporation to own the real estate in the United States. If the nonresident dies, the value of the shares of stock of the domestic corporation will be included in the gross estate, thereby causing U.S. estate tax.

(Shares of stock are “located” in the place of incorporation of the corporation; a stock of a U.S. corporation is therefore located in the United States, and thus the deceased shareholder owned an interest in “property” (stock of a domestic corporation) that was “situated” in the United States).

The nonresident can restructure this by transferring the domestic corporation stock by gift to a nongrantor trust. When everything is finished, ownership of the U.S. real estate is held in the following way:

Assume a competent job by the lawyer. The Settlor (who created the trust and transferred the corporate stock to the trust) does not hold a retained interest, and the Beneficiary does not have a general power of appointment.

Now both the Settlor and Beneficiary can rest easy, knowing that no U.S. estate tax will be imposed when they die.

Gift Tax

Nonresident-noncitizens of the United States (a different classification entirely from “nonresident alien”) are subject to U.S. gift tax – but only on gifts (to anyone) of two types of assets:

- Real estate situated in the United States; and

- Tangible personal property situated in the United States.

(Warning: law professors everywhere are spinning in their graves. What follows is an extremely hand-wavy approximation of the Law of Property. Do not rely on this as being anywhere close to authoritative.)

- Shares of corporate stock are “property.” It’s a thing you can own.

- There are two (and only two) types of property: “real property” (land and fixtures), and “personal property” (everything that’s not real property).

- Corporate stock is not real property, so it must be personal property.

- Personal property comes in two flavors: “tangible” personal property (you can actually touch it) and “intangible” personal property (everything else).

- You can’t touch a corporation, and you can’t touch the ownership rights of a corporation (shares). (A stock certificate is not the actual share of ownership. It’s a piece of paper that says you have an actual share of stock of the corporation.)

- Corporate stock is not “tangible” personal property, so it is intangible personal property.

Therefore, a gift of corporate stock (whether a foreign or domestic corporation) is a gift of intangible personal property. This is not one of the types of gifts that is subject to gift tax when made by a nonresident-noncitizen. The gift of stock of a domestic corporation to a nongrantor trust – even though the corporation owns U.S. real estate – is not a taxable gift.

From this, we can derive the following general planning principle:

an otherwise taxable gift by a nonresident-noncitizen can usually be converted into a tax-free gift by transferring ownership of the asset to an entity, and then giving away the ownership interests in that entity.

This concept works for partnership interests, LLC membership interests, and stock. If a nonresident wants to give U.S. real estate without paying gift tax, put the real estate into an entity first.

(Missing piece of information that will give you the full picture: a nonresident-noncitizen has a puny $13,000 unified credit that protects $60,000 of assets from U.S. estate tax.)

Domestic or foreign trust?

A trust used to hold U.S. real property can be domestic or foreign.

I prefer using a domestic trust for one simple reason: if something can go wrong, it will. And domestic trusts are less likely to “go wrong.”

- Section 643(i) says that a deemed distribution from a foreign nongrantor trust occurs if a U.S. person has rent-free use of trust-owned property. People do the damnedest things, like be nonresidents but have U.S. citizen children who they allow to live in the house. Section 643(i) does not apply to domestic trusts.

- Who knows what kind of exciting perturbations in the universe can happen in the future. Some of these may trigger a filing requirement for Form 3520 and Form 3520-A. These filing requirements apply to foreign trusts, not to domestic trusts. Why create a possibility for future penalties when Murphy’s Law rolls the cosmic dice?

- Section 684 applies to U.S. persons making transfers to foreign trusts. It creates a deemed sale, and I’ve seen these circumstances pop up just because people are living their ordinary lives. If the trust is domestic, Section 684 cannot possibly apply and force an unpleasant and unwanted capital gain recognition event.

- FIRPTA withholding is required when there is a sale of U.S. real estate by nonresidents. A domestic trust is a domestic taxpayer. No withholding requirements apply.

- Distributions to U.S. beneficiaries from a foreign trust are subjected to the throwback rules and accumulation distributions are subjected to punitive taxes.

The big problem with trusts

The big problem with trusts, of course, is that they are complicated, expensive, weird, and require the client to turn over control of a significant asset to a trustee.

But they are suited to the task

However, I like trusts. They are precisely the tool created for the job we want to do: hold an asset safely and securely, with predictable and acceptable estate and income tax results.

As we will see next time – starting with a discussion of income tax considerations – corporate structures create unpleasant or unknown income tax risks.

Corporations are designed for a group of people engaged in business activities, and repurposing them as holding vehicles for personal use assets means you’re using a screwdriver for a hammer’s job.

Conclusion/Next Time

That’s it for the estate tax considerations of a holding structure for a personal residence owned by a nonresident of the United States. In summary, to get estate tax protection:

- Use a holding structure that contains a foreign corporation; or

- Use a holding structure that contains a domestic or foreign nongrantor trust.