How much income is reported on this shareholder’s Form 1040? Why?

Why does Subpart F income jump directly from the bottom-level controlled foreign corporation to the United States shareholder’s Form 1040? Doesn’t it make more sense to pass the income item up the holding structure from subsidiary to parent to shareholder?

And what about cash? The cash dividends don’t jump – they follow the structure. How does that affect each entity – and the tax liability of the United States shareholder?

That’s what I’m covering in the next three episodes. I want to show a simple example of CFC operations and the impact on:

- Taxable income of the United States shareholder;

- Basis in the stock; and

- Earnings and profits.

In this episode:

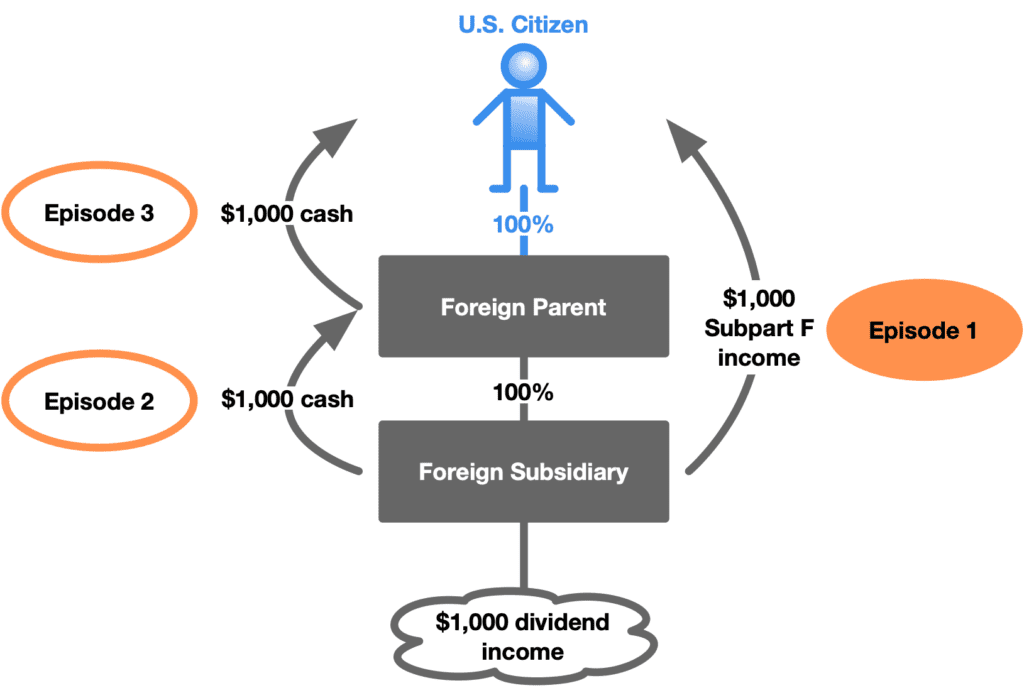

- Episode 1 – how Subpart F income leaps onto the tax return of a shareholder whose name is not on a stock certificate of the corporation.

In upcoming episodes:

- Episode 2 – how to report a cash distribution from a foreign subsidiary to a foreign parent.

- Episode 3 – how a cash distribution from a CFC to its direct U.S. shareholder affects the U.S. shareholder’s gross income (or, when is a dividend not a dividend?).

Over the course of these three episodes, I will touch on:

- IRC §301(c) – how a shareholder is taxed on corporate distributions

- IRC §951(a) – inclusion of Subpart F income in a U.S. shareholder’s gross income

- IRC §952 – the definition of Subpart F income generally

- IRC §954 – why dividend income is foreign personal holding company income is foreign base company income is Subpart F income

- IRC §958(a)(2) – the meaning of indirect ownership of foreign corporations’ stock

- IRC §959 – when distributions of earnings and profits are or are not included in the U.S. shareholder’s gross income

- IRC §961 – basis adjustments for Subpart F inclusions and CFC distributions

- IRC §964(a) – earnings and profits calculations for CFCs.

LFG.

Facts for this episode

A U.S. citizen owns 100% of the stock of Foreign Parent, which in turn owns 100% of the stock of Foreign Subsidiary. Foreign Subsidiary receives $1,000 of dividend income from a publicly-traded company.

Question (and answer)

Q: How is Foreign Subsidiary’s $1,000 dividend income reflected on U.S. Citizen’s Form 1040?

A: U.S. Citizen includes Foreign Subsidiary’s $1,000 of dividend income on his Form 1040, as Subpart F income.

Foreign Subsidiary has Subpart F income

First things first: Subpart F income exists. Foreign Subsidiary, which received $1,000 of dividend income from ownership of publicly-traded stock, has Subpart F income.

Foreign Subsidiary, because it has $1,000 of dividend income, has $1,000 of Subpart F income:

- Dividend income is one of the components of foreign personal holding company income. IRC §954(c)(1)(A).

- Foreign personal holding company is one of the components of foreign base company income. IRC §954(a)(2).

- Foreign base company income is one of the components of Subpart F income. IRC §952(a)(2).

U.S. Citizen gross income includes the Subpart F income

- Question: When does a United States shareholder have inclusion of subpart F income in its/his her gross income?

- Answer: When the United States shareholder “owns (within the meaning of section 958(a)) stock in such corporation . . . .”

IRC §951(a)(1)(A) says (emphasis added):

If a foreign corporation is a controlled foreign corporation at any time during any taxable year, every person who is a United States shareholder (as defined in subsection (b)) of such corporation and who owns (within the meaning of section 958(a)) stock in such corporation on the last day, in such year, on which such corporation is a controlled foreign corporation shall include in his gross income, for his taxable year in which or with which such taxable year of the corporation ends—

(A) his pro rata share (determined under paragraph (2)) of the corporation’s subpart F income for such year[.]

A United States shareholder can own foreign corporation stock “within the meaning of section 958(a)” by:

- Direct ownership–a stock certificate says “United States shareholder” on it. (Not applicable in my example). IRC §958(a)(1)(A).

- Indirect ownership–the United States shareholder has an ownership interest in a foreign entity that owns the foreign corporation stock. (This is precisely my example). IRC §§958(a)(1)(B), 958(a)(2).

Indirect ownership is defined in IRC §958(a)(2) which reads, in its complete and overly-verbose form, as follows:

For purposes of subparagraph (B) of paragraph (1), stock owned, directly or indirectly, by or for a foreign corporation, foreign partnership, or foreign trust or foreign estate (within the meaning of section 7701(a)(31)) shall be considered as being owned proportionately by its shareholders, partners, or beneficiaries. Stock considered to be owned by a person by reason of the application of the preceding sentence shall, for purposes of applying such sentence, be treated as actually owned by such person.

Edited/simplified to take out all of the irrelevant words:

. . . [S]tock owned[ ] directly . . . by . . . a foreign corporation . . . shall be considered as being owned proportionately by its shareholders. . . .

By the power of basic middle school algebra (substituting a fixed value for a variable) we can solve the equation:

. . . [S]tock owned[ ] directly . . . by . . . Foreign Parent . . . shall be considered as being owned proportionately by U.S. Citizen. . . .

Foreign Parent owns 100% of Foreign Subsidiary’s stock. Therefore, U.S. Citizen is considered as indirectly owning 100% of Foreign Subsidiary’s stock, as “ownership” is defined in IRC §958(a).

We have applied IRC §958(a) to come to that conclusion, so we must follow IRC §951(a)(1)(A)’s strict orders and include Foreign Subsidiary’s Subpart F income in U.S. Citizen’s gross income.

Foreign Subsidiary’s earnings and profits

Just because I’m a teensy bit OCD (as a productivity hack, not as a way of life) let’s see what happens to Foreign Subsidiary’s earnings and profits. This will become important in Episode 2, when Foreign Subsidiary makes a distribution of the $1,000 cash to Foreign Parent.

The rule is stated at IRC §964(a), but the useful stuff is in Reg. §1.964-1. In a nutshell:

- Pretend that the foreign corporation is a domestic corporation and prepare a profit and loss statement. Reg. §1.964-1(a)(1)(i).

- Make accounting adjustments as specified in Reg. §1.964-1(b). Reg. §1.964-1(a)(1)(ii).

- Make tax adjustments as specified in Reg. §1.964-1(c). Reg. §1.964-1(a)(1)(iii).

- Make the little fiddly adjustments demanded by arcane rules in the Internal Revenue Code. Reg. §1.964-1(a)(2).

I have deliberately wildly oversimplified the facts to make the example easy, so here is my wildly oversimplified calculation of Foreign Subsidiary’s earnings and profits:

Next time, in Episode 2, we will see the effect on earnings and profits of the distribution of $1,000 by Foreign Subsidiary to its sole shareholder, Foreign Parent.

Basis adjustment in an unexpected place

IRC §961 is where we find the basis adjustment rules for CFCs. Wildly oversimplified: Subpart F income inclusions increase basis (IRC §961(a)), and distributions (sometimes) decrease basis in the CFC stock (IRC §961(b)).

This oversimplification is incomplete and wrong, but I say it out loud because I kept that mental model in my head and thereby confused myself for too long. Don’t do what I did. Read this explanation, then read IRC §961, then you will have an accurate understanding of the basis adjustment rules.

Here’s how “I didn’t bother to read the Code” can lead you astray (and remember, I am raising my hand as one of the guilty non-readers). In my example, U.S. Citizen will take Subpart F income of Foreign Subsidiary into gross income. That means basis in Foreign Subsidiary stock should go up.

- (Insert Puzzled Phil Brain Here). But U.S. Citizen does not own Foreign Subsidiary stock. How can you have a basis adjustment to an asset you do not own?

Reading IRC §961(a) makes it all clear: in situations of indirect ownership of a CFC, adjust the basis of the entity ownership interest that you actually own in the holding structure that in turn owns the CFC stock.

Under regulations prescribed by the Secretary, . . . the basis of property of a United States shareholder by reason of which he is considered under section 958(a)(2) [editor’s note: that’s the “indirect ownership through a foreign entity” rule] as owning stock of a controlled foreign corporation, shall be increased by the amount required to be included in his gross income under section 951(a) . . . with respect to such property, as the case may be, but only to the extent to which such amount was included in the gross income of such United States shareholder. * * *

U.S. Citizen owns “property” in the form of Foreign Parent stock. Through ownership of that property, U.S. Citizen is treated as owning Foreign Subsidiary stock, a controlled foreign corporation and the source of amounts included in gross income because of IRC §951(a).

Therefore, U.S. Citizen adjusts basis of Foreign Parent stock upward by the amount of Subpart F income included in gross income from Foreign Subsidiary.

This will be the key to putting $1,000 cash into U.S. Citizen’s pocket in Episode 3, without having that cash be treated as dividend income from Foreign Parent.

Cliffhanger

That’s the first step in analysis of how to pass Subpart F income from a lower-tier CFC to a United States shareholder. The important principles:

- Subpart F Income. Compute the lower-tier CFC’s Subpart F income in the usual fashion.

- Earnings and Profits. Compute earnings and profits calculations for the lower-tier CFC in the usual way.

- Allocate Subpart F Income. Apply the indirect ownership principles of IRC §958(a)(2) and allocate the lower-tier CFC’s Subpart F income to the first U.S. shareholder you find when applying IRC §958(a)(2).

- Shareholder’s Gross Income. The shareholder has gross income inclusion because of IRC §951(a).

- Stock Basis Adjustment. Look at the holding structure and identify the top-tier foreign entity in which the United States shareholder has an ownership interest. In this case, U.S. Citizen owns 100% of Foreign Parent’s stock. Increase the U.S. shareholder’s basis in that ownership interest (in this case, Foreign Parent stock) by the amount of Subpart F income included in the U.S. shareholder’s gross income.

In Episode 2, I will show what happens to Foreign Subsidiary, Foreign Parent, and U.S. Citizen when Foreign Subsidiary pays a $1,000 dividend to its sole shareholder–Foreign Parent.

Stay tuned for the next thrilling episode, in two weeks.

Request

Email me please.

Tell me what topics (Form 5471 or otherwise) would be useful to you. Tell me a bit about yourself.

Sometimes it gets a bit lonely and isolated here, blasting emails out into the internet. I’d like to get to know as many of you as possible.

Phil.