Back to U.K. SIPPs – Highly Compensated Employees

Welcome Back

I’m Phil Hodgen, your international tax impresario.

Vacation

I’ve been away. Three weeks in Portugal almost entirely offline. (A week in Porto, a week riding an electric bike down the coast from Porto to Óbidos, then a week in Lisbon. Unsolicited and uncompensated recommendation: Exodus Adventure Travels–here is the trip I did with my wife and friends. Try to get João Colaço as your travel guide.

London 2026

Then I spent almost two weeks in London.

There, we held the Second Annual London International Tax Summit on June 26, 2026, and a half-day Business of Practice workshop on June 27, 2026, focusing on AI for professional services firms. Top tier, and many, many happy comments.

The international tax community is surprisingly small. Many of us are sole practitioners or in small firms. It’s wonderful to get to know so many of you around the world. Thanks for attending the events and the social events at the pub on Thursday and Friday nights.

Save the Date for London 2027

Save the date for the 2027 events in London:

- Third Annual London International Tax Summit: June 25, 2027. Chartered Accountants Hall, 1 Moorgate Place.

- Business of Practice workshop (again will be heavily AI): June 26, 2027. Probably the same co-working space we used this year, Soho Works, 180 Strand.

Any Interest in a Milan Event?

I will be in Milan this September and again in February 2027. (My wife attends the White Show).

Email me if you’re interested in attending an international tax event in Milan in the last week of February, 2027. The usual format is enough technical background to justify CPE credits and a business expense deduction, then plenty of socializing. If there’s enough interest, I will create a program.

Join the International Tax Pros

The London International Tax Summit and the AI workshop were/are part of the International Tax Pros community’s activities. You should be a member. We are friendly and generous people. If that’s you, please consider joining.

OK, enough chit-chat. Let’s get down to technical brass tacks. It’s back to the UK SIPP project and a sprint to finish off the Field Guide I’m writing.

Part 1 retrospective: we know the SIPP’s entity type

Part 1 of the Field Guide for U.K. SIPPs is complete in rough draft, having been published here and there in this newsletter over the last several months. I may get energetic and throw the rough draft up on the website. 🙂

In Part 1, I walked you through the analysis of figuring out what type of entity the Internal Revenue Code thinks a SIPP is. There are three possible answers:

- a foreign grantor trust;

- a nonexempt foreign employees’ trust (as that term is used in IRC section 402(b)); or

- partly foreign grantor trust and partly nonexempt foreign employees’ trust.

Part 2 preview: how the Internal Revenue Code taxes U.S. members of U.K. SIPPs

There are two sets of tax laws under which a U.S. member of a U.K. SIPP can determine his or her U.S. income tax obligations: the Internal Revenue Code (Part 2 of the Field Guide) or the U.K./U.S. Income Tax Treaty (upcoming Part 3 of the Field Guide).

Part 2 of the Field Guide is where we are right now, and what you’re going to see for the next few installments of The Friday Edition. Part 2 explores the Internal Revenue Code’s default treatment of contributions to and distributions from a U.K. SIPP to a U.S. member, as well as the treatment of investment earnings on the SIPP’s assets. Since there are three possible classifications for a SIPP (see the three outcomes from Part 1) there will be three sections of Part 2:

- Part 2.1: Taxation of SIPP members when the SIPP is a foreign employees’ trust

- Part 2.2: Taxation of SIPP members when the SIPP is a foreign grantor trust

- Part 2.3: Taxation of SIPP members when the SIPP is a bifurcated foreign employees’ trust

Let’s begin with the hardest one: the foreign employees’ trust.

Part 2.1: how the Internal Revenue Code taxes members of SIPPs that are foreign employees’ trusts

Taxation of employees who are participants in foreign employees’ trusts is dictated by the rules in IRC §402(b). There are default rules and there are exceptions. The exceptions are toggled by two facts:

- whether the SIPP member a “highly compensated employee” and

- whether the SIPP fails to meet “coverage” tests (i.e., it unfairly excludes rank-and-file employees).

That is what I will be exploring in Part 2.1. The chapters (tentatively) in Part 2.1 are organized like this:

- Exceptions. Paradoxically, I start with the exceptions, not the general rules. There are two exceptions at IRC §402(b)(4) that override the default rules for taxation of contributions, distributions, and investment earnings. I provide a roadmap for you to figure out if the exceptions apply to you. If they apply, I explain how your SIPP member is taxed on contributions, distributions, and investment earnings.

- Contributions. How is the SIPP member taxed on employer contributions to the SIPP? This is a discussion of IRC §402(b)(1).

- Distributions. How is the the SIPP member taxed on distributions received? This is a discussion of IRC §402(b)(2).

- Investment Earnings. There is no explicit rule in IRC §402(b) that describes how a SIPP member is (or is not) taxed on investment earnings inside a SIPP prior to distribution. Using cunning logic, the conclusion will be that the employee is not subject to U.S. income tax on investment earnings prior to distribution.

Plus bumpers: an introduction at the front to give you a mental roadmap, and summary at the end to wrap up what we discussed.

Let’s start with the first half of the chapter about the IRC §402(b)(4)(A) exception for highly compensated employees.

Exception: IRC §402(b)(4)(A) for highly compensated employees

Employees who are participants in a nonexempt foreign employees’ trust (a SIPP member is such a person) have their tax lives controlled by IRC §402(b). The general rules for taxation are at IRC §402(b)(1) and (2), and the two exceptions to the general rules are at IRC §402(b)(4)(A) and (B).

Let’s start with the exception at IRC §402(b)(4)(A):

If 1 of the reasons a trust is not exempt from tax under section 501(a) is the failure of the plan of which it is a part to meet the requirements of section 401(a)(26) or 410(b), then a highly compensated employee shall, in lieu of the amount determined under paragraph (1) or (2) include in gross income for the taxable year with or within which the taxable year of the trust ends an amount equal to the vested accrued benefit of such employee (other than the employee’s investment in the contract) as of the close of such taxable year of the trust.

Note that this exception is keyed to apply to highly compensated employees. It will potentially apply to many SIPP members who are not highly compensated by any measure. Someone who owns more than 5% of the employer is a highly compensated employee. Thus, a U.S. citizen who is the sole shareholder of a limited company and pays himself a princely £5,000 per annum is a “highly compensated employee” squarely in the target of this exception.

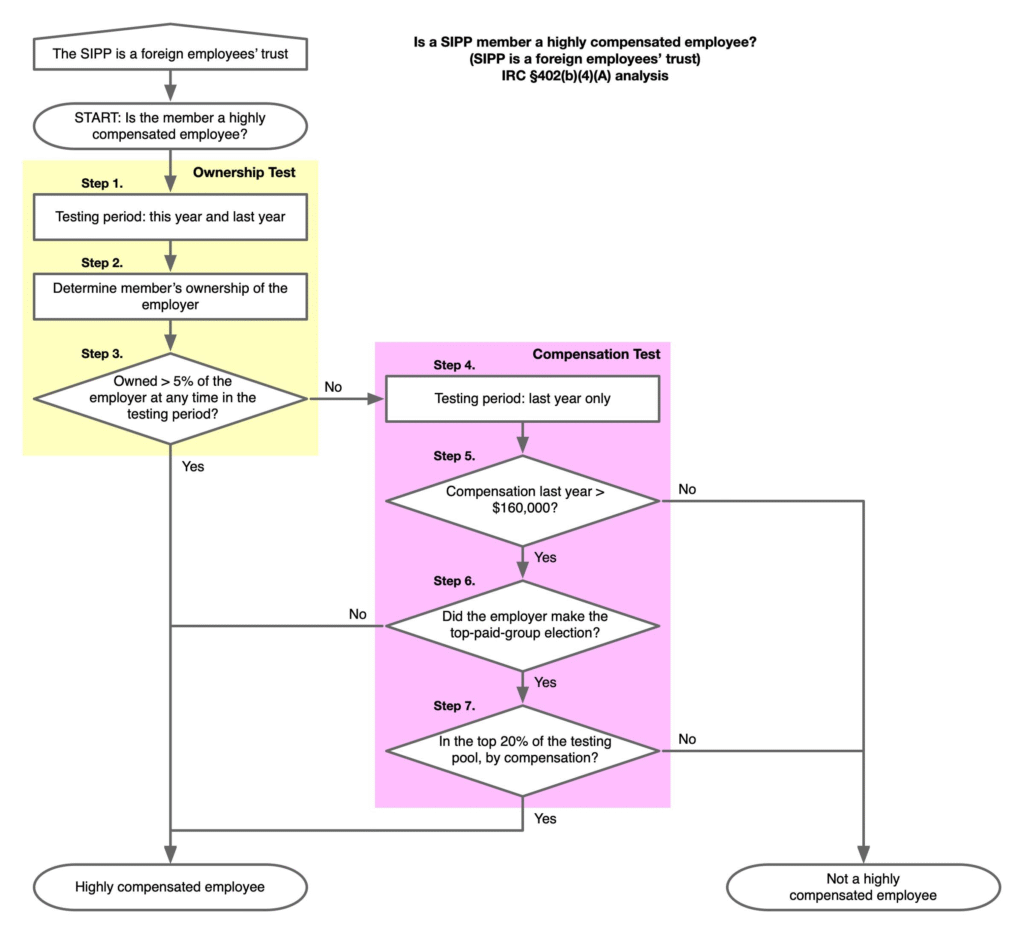

Here is a flowchart showing how you figure out whether a SIPP member is a highly compensated employee. I will walk through the steps one at a time.

If you determine that your SIPP member is NOT a highly compensated employee, the exception at IRC §402(b)(4)(A) does not apply and the general rules of IRC §402(b)(1) and (2) will govern U.S. taxation of the SIPP member’s contributions and distributions.

If you determine that your SIPP member IS a highly compensated employee, your analysis might not be over. In order to determine whether your SIPP member is captured by the IRC §402(b)(4)(A) exception, you may need to look at the SIPP to see if it unfairly discriminates against rank-and-file (non-highly compensated) employees.

Start: Highly compensated employee

Here is your flowchart for figuring out whether a SIPP member is a highly compensated employee, as that phrase is defined for purposes of IRC §402(b).

Download the diagram here as a PDF file.

“Highly compensated employee” is defined in IRC §402(b)(4)(C) by cross-reference to IRC §414(q).

IRC §414(q)(1) defines “highly compensated employee” by a stock ownership test or a total compensation test.

Start with the stock ownership test, because it frequently is a short-cut to highly compensated employee status.

The Ownership Test

This is the yellow-shaded area on the flow chart.

Step 1. Determine testing period for the ownership test

The first way to be a highly compensated employee is by owning more than 5% of the employer. To do this analysis, you first determine the testing period. Then you look at every moment during the testing period to determine whether the SIPP member’s ownership exceeded the 5% threshold.

IRC §414(q)(1)(A) says that your SIPP member will be a “highly compensated employee” if the ownership threshold is met for the current and previous years:

The term “highly compensated employee” means any employee who—`

(A) was a 5-percent owner at any time during the year or the preceding year[.]

Step 2. Determine ownership percentage

Next, do some fact gathering and math to determine whether, during the testing period, the SIPP member owned enough of the employer to pass the 5% threshold.

“Five-percent owner” is defined in IRC §414(q)(2) by incorporating the definition in IRC §416(i)(1) by reference. In turn, IRC §416(i)(1)(B)(i) says:

For purposes of this paragraph, the term “5-percent owner” means—

(I) if the employer is a corporation, any person who owns (or is considered as owning within the meaning of section 318) more than 5 percent of the outstanding stock of the corporation or stock possessing more than 5 percent of the total combined voting power of all stock of the corporation, or

(II) if the employer is not a corporation, any person who owns more than 5 percent of the capital or profits interest in the employer.

The definition of “5-percent owner” a bit of a classic tax breadcrumbs game:

- IRC §402(b)(4)(C) points you to

- IRC §414(q), which defines 5-percent owner at

- IRC §414(q)(2) by cross reference to

- IRC §416(i)(1), where at

- IRC §416(i)(1)(B)(i) you find the exact definition you need.

The Regulations are a similar bouncy-house experience.

- Reg. §1.414(q)-1, the final regulation that we would invoke because we were sent to IRC §414(q), is almost entirely “Reserved.” It says nothing about 5-percent owners, and instead points you at the temporary regulations at Reg. § 1.414(q)-1T.

- Reg. §1.414(q)-1T A-8 defines 5% owner, but expressly “as defined in section 416(i)(B)(i) and § 1.416-1 A T-17&18.” Another pointer.

- Reg §1.416-1 T-16 / T-17 / T-18 is where we finally find the operative content: the >5% test, the IRC §318 attribution, and the “IRC §414(b)/(c)/(m) don’t aggregate” rule.

I take this little detour to encourage you to be suitably anal-retentive and OCD in your approach to tax research. This is the way the IRS figures things out, so you should, too.

Learn to follow the breadcrumbs and never miss a step. If you know how to do this, you will be more likely to catch your favorite AI when it does not follow the breadcrumbs and comes to a wrong conclusion. It happens.

Step 3. Above the 5% threshold? Yes/no

Step 3 is simple: is the ownership you calculated at Step 2 above the 5% threshold?

- If yes, the SIPP member is automatically a highly compensated employee. The actual amount of compensation received is irrelevant.

- If no, the SIPP member is not automatically a highly compensated employee because of the ownership test, but has the possibility of being a highly compensated employee based on the compensation test. You need to do Steps 4-7 to determine if the SIPP member is a highly compensated employee.

If Necessary, the Compensation Test

The compensation test portion of the analysis is shown in the purple-shaded portion of the flow chart. I will walk you through the compensation test next time. It looks complicated (especially that little thing about an employer election). But in fact in real life the complexity never happens with a SIPP so it’s a straightforward analysis.

Email me

Email me if you’re interested in attending an international tax event in Milan in the last week of February, 2027. Or just say hi.