Form 5471 and Form 5472 required? How to eliminate Form 5472

Hello once again and welcome to The Friday Edition: an every-other-Friday newsletter with international tax information for people who do this stuff for a living. I’m Phil Hodgen. I do this stuff for a living.

When you have to file Form 5471 and Form 5472

Sometimes you have a situation where you need to prepare both Form 5471 and Form 5472. Here is a discussion of an exception that allows you to eliminate Form 5472.

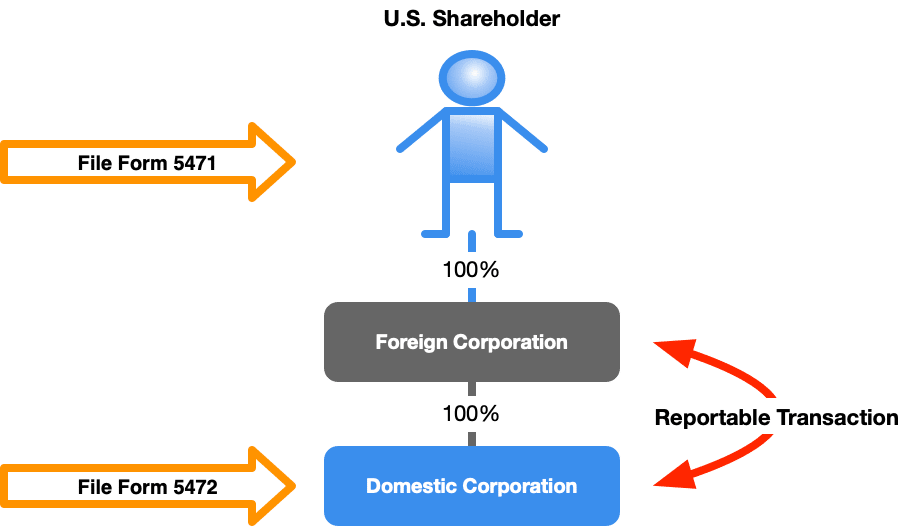

Example: a U.S. citizen owns 100% of the stock of a foreign corporation, which in turn owns 100% of a domestic corporation.

When you don’t have to file Form 5472

There are six exceptions that can eliminate a Form 5472 filing obligation. You can see them listed in Instructions for Form 5472 (Rev. 12-2024) on page 2. One of the exceptions applies to situations just like this.

Reg. § 1.6038A-2(e)(3)

Here’s the Regulation:

Reg. § 1.6038A-2(e)(3) Transactions with a Corporation Subject to Reporting Under Section 6038. A reporting corporation (other than an entity that is a reporting corporation as a result of being treated as a corporation under § 301.7701-2(c)(2)(vi) of this chapter) is not required to make a return of information on Form 5472 with respect to a related foreign corporation for a taxable year for which a U.S. person that controls the foreign related corporation makes a return of information on Form 5471that is required under section 6038 and this section, if that return contains information required under § 1.6038-2(f)(11) with respect to the reportable transactions between the reporting corporation and the related corporation for that taxable year. Such a reporting corporation also is not subject to section 1.6038A-3 and 1.6038A-5. It remains subject to the general record maintenance requirements of section 6001.

Instructions for Form 5472 (Rev. 12-2024)

The Instructions for Form 5472 (Rev. 12-2024) give a pretty good explanation of this exception:

A reporting corporation is not required to file Form 5472 if any of the following apply.

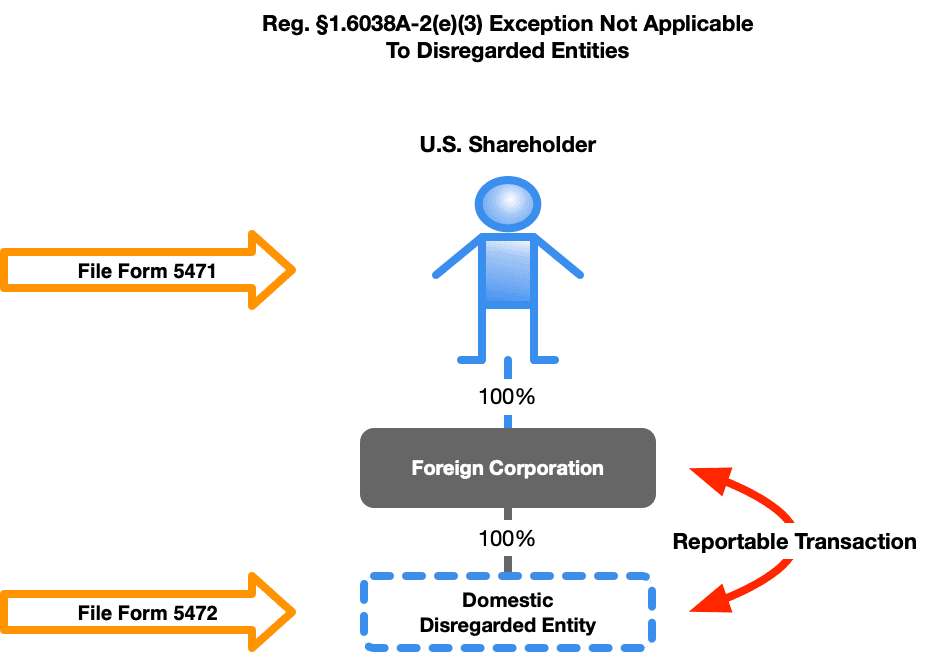

- A U.S. person that controls the foreign related corporation files Form 5471, Information Return of U.S. Persons With Respect to Certain Foreign Corporations, for the tax year to report information under section 6038. To qualify for this exception, the U.S. person must complete Schedule M (Form 5471) showing all reportable transactions between the reporting corporation and the related party for the tax year. This exception does not apply to foreign-owned U.S. DEs.

The exception discussed here eliminates Form 5472 filing obligation ONLY eliminated for:

- A foreign related corporation (that’s a foreign corporation that is “related” to the domestic corporation; see IRC §6038A(c)(2)).

- That is controlled (more than 50% owned; see IRC §6038(e)(2)) by a U.S. person.

- Who files Form 5471 for that foreign corporation.

- And includes Schedule M (Form 5471).

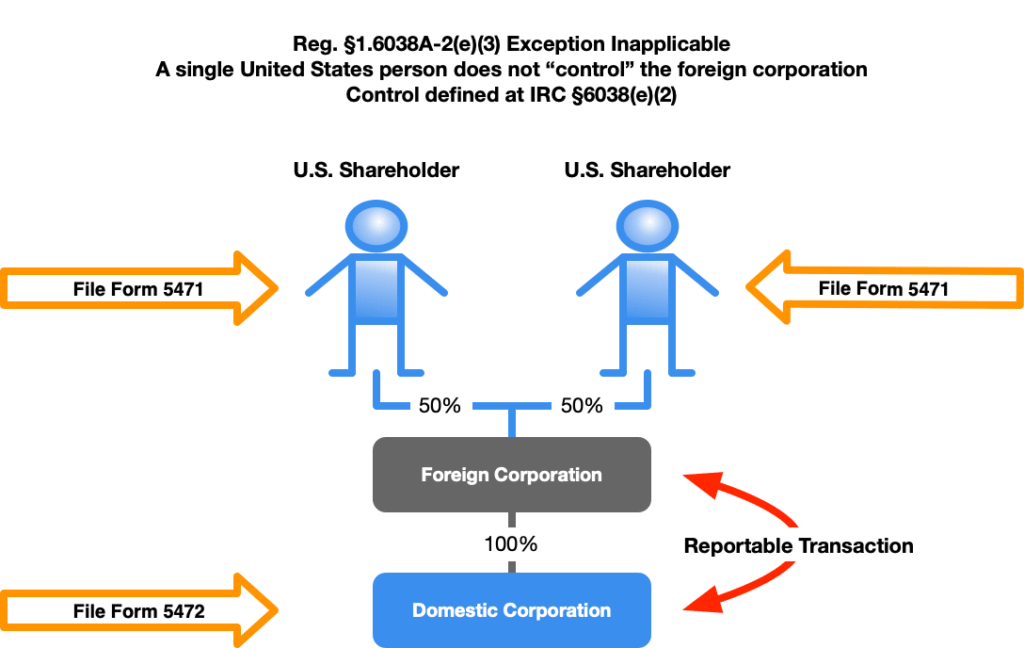

No “control” by one U.S. person? No Form 5472 exception

A United States person must “control” the foreign related corporation. That is the prerequisite for this exception (emphasis added):

Reg. § 1.6038A-2(e)(3) Transactions with a Corporation Subject to Reporting Under Section 6038. A reporting corporation (other than an entity that is a reporting corporation as a result of being treated as a corporation under § 301.7701-2(c)(2)(vi) of this chapter) is not required to make a return of information on Form 5472 with respect to a related foreign corporation for a taxable year for which a U.S. person that controls the foreign related corporation makes a return of information on Form 5471that is required under section 6038 and this section, if that return contains information required under § 1.6038-2(f)(11) with respect to the reportable transactions between the reporting corporation and the related corporation for that taxable year. Such a reporting corporation also is not subject to section 1.6038A-3 and 1.6038A-5. It remains subject to the general record maintenance requirements of section 6001.

Note that the person who has control is defined in the singular: “a” U.S. person.

A person “controls” a foreign corporation when he or she owns more than 50% of the foreign corporation’s stock, by vote or value. IRC §6038(e)(2). Here’s an example of a situation where no U.S. person “controls” the foreign corporation:

The foreign corporation is owned by two U.S. persons, each holding 50% of the stock. Neither U.S. person controls the foreign corporation. It is a controlled foreign corporation, and each U.S. shareholder has a Form 5471 filing obligation. It is a foreign related corporation for Form 5472 purposes, and there is a reportable transaction. Therefore it has a Form 5472 filing obligation.

The Form 5472 filing exception does not apply, because a U.S. person, alone, does not “control” the foreign corporation because there is no “greater than 50%” shareholder. The Reg. §1.6038A-2(e)(2) fails.

The exception doesn’t apply to disregarded entities

The exception does not apply where a foreign corporation owns a domestic disregarded entity. The Regulation states (emphasis added):

Reg. § 1.6038A-2(e)(3) Transactions with a Corporation Subject to Reporting Under Section 6038. A reporting corporation (other than an entity that is a reporting corporation as a result of being treated as a corporation under § 301.7701-2(c)(2)(vi) of this chapter) is not required to make a return of information on Form 5472 with respect to a related foreign corporation for a taxable year for which a U.S. person that controls the foreign related corporation makes a return of information on Form 5471 that is required under section 6038 and this section, if that return contains information required under § 1.6038-2(f)(11) with respect to the reportable transactions between the reporting corporation and the related corporation for that taxable year. Such a reporting corporation also is not subject to section 1.6038A-3 and 1.6038A-5. It remains subject to the general record maintenance requirements of section 6001.

Summary

In short, use this exception to eliminate Form 5472 filing obligations where:

- That foreign corporation is “related” to the reporting corporation (the domestic corporation but not disregarded entity).

- There is a reportable transaction between the domestic corporation and the foreign corporation.

- One United States person “controls” a foreign corporation—i.e., owns more than 50% of its stock by vote or value. This is the potential “gotcha” in the exception. It doesn’t mean “controlled foreign corporation” because that could mean more than one shareholder. the exception demands a foreign corporation that is “controlled” by one U.S. person.

- The United States person files Form 5471 and attaches Schedule M (Form 5471).

For all other situations, find another exception to eliminate Form 5472 filing obligations, or . . . file Form 5472.