OBBBA: no more downward attribution and the brand new IRC section 951B

Hello and welcome once again to The Friday Edition. Every other Friday, more international tax fun from me, Phil Hodgen.

If someone forwarded this newsletter to you, please subscribe for your own copy straight to your inbox. Sign up at internationaltaxlaw.com.

Watch a bunch of international tax videos on YouTube. Maybe even join the International Tax Pros–a community of accountants, enrolled agents, and attorneys who do lots of international tax stuff in their day jobs.

Strap in for a bit of a ride. This is an overview of two provisions from the One Big Beautiful Bill (OBBBA).

One change means that fundamental questions may now have new answers, thanks to “no more downward attribution” caused by the restoration of IRC §958(b)(4):

- Who is a U.S. shareholder?

- When is a foreign corporation a controlled foreign corporation?

The other change discussed here is new IRC §951B, which created a whole new class of taxpayers who are a risk of income inclusions for subpart F income and net CFC tested income.

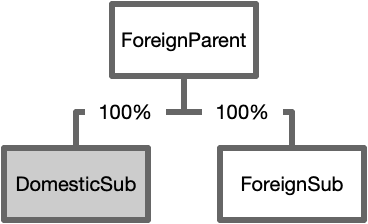

Example 1: IRC §958(a)(4) existed, was repealed, and has been restored

Assume this structure:

Before the TCJA (2017)

Before TCJA, IRC §958(b)(4) existed, prohibiting downward attribution by blocking the application of IRC §318(a)(3).

Domestic Sub would not be a United States shareholder of ForeignSub. DomesticSub’s stock ownership in ForeignSub is determined by applying the rules of IRC §958(a), (b). IRC §951(b). Application of those rules results in zero percent ownership:

- DomesticSub did not own any ForeignSub stock directly. IRC §958(a)(1)(A).

- DomesticSub did not own any ForeignSub stock indirectly through foreign entities. IRC §958(a)(1)(B), (a)(2).

- DomesticSub did not own any ForeignSub stock constructively by application of the IRC §318(a) rules. IRC §958(a)(4), as it existed before the TCJA, probihited the use of the downward attribution rules of IRC §318(a)(3), so DomesticSub was not treated as owning ForeignSub stock owned by ForeignParent.

ForeignSub would not be a controlled foreign corporation. A controlled foreign corporation is a foreign corporation that is more than 50% owned by United States shareholders. IRC §957(a). ForeignSub is 100% owned by ForeignParent—no United States shareholders exist. Therefore, ForeignSub, prior to the TCJA, would not have been a controlled foreign corporation.

Since income inclusions for subpart F income applied only to United States shareholders of controlled foreign corporations (IRC §951(a)), DomesticSub would have no income inclusion because it was not a United States shareholder and ForeignSub was not a controlled foreign corporation. (There would be no income inclusion for global intangible low-taxed income because that wasn’t a thing prior to the TCJA).

TCJA to OBBBA (2018 – 2025)

The TCJA repealed IRC §958(a)(4). Repeal meant that downward attribution could then be used to figure out the key status questions of “am I a United States shareholder?” and “is this foreign corporation a controlled foreign corporation?”

From 2018 through 2025, DomesticSub was classified as a United States shareholder. Again, we determine stock ownership by applying the rules of IRC §958(a), (b). IRC §951(b). When we do so, we find that DomesticSub owns 100 percent of ForeignSub’s stock:

- DomesticSub did not own any ForeignSub stock directly. IRC §958(a)(1)(A).

- DomesticSub did not own any ForeignSub stock indirectly through foreign entities. IRC §958(a)(1)(B), (a)(2).

- DomesticSub owns 100 percent of ForeignSub stock constructively by application of the IRC §318(a) rules. IRC §958(a)(4) did not exist, so we applied the downward attribution rule of IRC §318(a)(3)(C) to treat DomesticSub as owning all of the ForeignSub stock owned by ForeignParent.

Similarly, ForeignSub was a controlled foreign corporation. IRC §957(a). One United States shareholder (DomesticSub) owned 100 percent of ForeignSub’s stock because of the IRC §958(b) stock ownership rule.

ForeignSub would have no income inclusions, however. Income inclusions occur only to the extent that a United States shareholder has direct (IRC §958(a)(1)(A)) or indirect through foreign entities (IRC §958(a)(1)(B), (a)(2)) ownership of CFC stock, and in this case DomesticSub has neither.

2026 and future

The OBBBA reinstated IRC §958(b)(4). Effective for tax years starting after December 31, 2025, “no downward attribution” is what’s for dinner. As a result, we are back to the way things were before the TCJA: DomesticSub is not a United States shareholder and ForeignSub is not a controlled foreign corporation.

- DomesticSub does not own any ForeignSub stock directly. IRC §958(a)(1)(A).

- DomesticSub does not own ForeignSub stock indirectly through foreign entities. IRC §958(a)(1)(B), (a)(2).

- DomesticSub does not own ForeignSub stock constructively under the IRC §318(a) rules because IRC §958(a)(4) prohibits application of the downward attribution rules of IRC §318(a)(3)(C). IRC §958(b).

- ForeignSub is not a controlled foreign corporation because it has no United States shareholders, therefore it is impossible for United States shareholders to own more than 50 percent of its stock. IRC §957(a).

This means less compliance burden. While there are filing exceptions that excused taxpayers like DomesticSub from filing Form 5471 under various categories, some gratuitous paperwork requirements still existed. Now, it will be impossible for a Form 5471 filing requirement to apply in this situation because all categories require a United States shareholder in some fashion, and there is no United States shareholder in this common corporate structure.

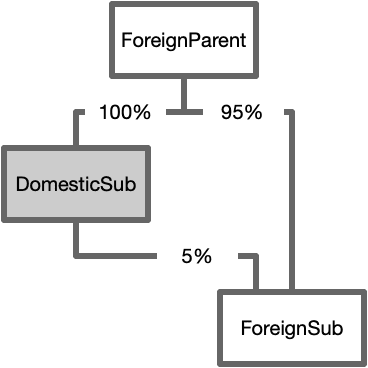

Example 2: direct and constructive ownership structures

Consider a different structure, where DomesticSub owns five percent of ForeignSub stock directly. ForeignParent owns the other 95 percent of ForeignSub stock.

Before 2017: no income inclusion

Before 2017, DomesticSub would not have been a United States shareholder of ForeignSub, because its five percent direct stock ownership is less than the threshold 10 percent ownership required for United States shareholder status. No constructive ownership of stock would occur because IRC §958(a)(4) blocked application of the downward attribution rule of IRC §318(a)(3)(C).

Therefore, DomesticSub would be safe from a subpart F income inclusion from ForeignSub. (Global intangible low-taxed income did not exist before the TCJA).

2018 – 2025: income inclusion

After TCJA, DomesticSub would have a subpart F income and a global intangible low-taxed income inclusion problem. IRC §958(a)(4) had been removed, allowing downward attribution of ForeignParent’s 95 percent stock ownership in ForeignSub to DomesticSub.

As a result, DomesticSub became a United States shareholder owning 100 percent of ForeignSub’s stock: five percent directly and 95 percent constructively. And, ForeignSub was a controlled foreign corporation: all of its stock was owned by a single United States shareholder.

ForeignSub’s subpart F income and global intangible low-taxed income would, during this time period, be allocated pro rata to United States shareholders based on their stock ownership under IRC §958(a)—directly-owned or indirectly-owned stock. IRC §§951(a)(2), 951A(e)(1).

DomesticSub owned five percent of ForeignSub’s stock directly. Therefore, five percent of ForeignSub’s subpart F income and global intangible low-taxed income would be included in DomesticSub’s gross income.

2026 and future: no income inclusion (but look at IRC §951B)

Starting with tax years beginning after December 31, 2025, DomesticSub will no longer be a United States shareholder. It owns five percent of ForeignSub’s stock directly, but does not own ForeignParent’s 95 percent of ForeignSub’s stock constructively because newly-restored IRC §958(a)(4) prohibits downward attribution of ForeignParent’s stock holdings to DomesticSub.

Similarly, ForeignSub is no longer a controlled foreign corporation. It does not have any United States shareholders (United States persons who own 10 percent or more of its stock). IRC §957(a).

Therefore, under the classic income inclusion rules for subpart F income and net CFC tested income (the new name for global intangible low-taxed income), DomesticSub will not have any income of ForeignSub included in its gross income.

IRC §951B: 2026 and future: income inclusions for a new class of taxpayers

That would be an entirely fine result. It returns us to the good old days before the TCJA.

Unfortunately, that’s not what happened with the OBBBA.

The OBBBA gave us brand new IRC §951B, adding a nugget of complexity and creating a new class of taxpayers to whom IRC §951(a) (subpart F income inclusion) and IRC §951A(a) (net CFC tested income inclusion) will apply.

- You don’t have to be a United States shareholder (IRC §951(b) definition) anymore to have income attributed to you from a foreign corporation.

- And the foreign corporation that creates an income inclusion for you doesn’t need to be a controlled foreign corporation (IRC §957(a) definition).

IRC §951B creates new, special-purpose types of United States shareholders and controlled foreign corporations:

- “United States shareholder” becomes “foreign controlled United States shareholder.”

- “Controlled foreign corporation” becomes “foreign controlled foreign corporation.”

If both special definitions apply, IRC §951B applies most of subpart F (IRC sections 951 through 965) to cause affected taxpayers to have income inclusions under IRC §951(a) and IRC §951A(a)—even if the taxpayer is not a United States shareholder and the foreign corporation is not a controlled foreign corporation according to the standard definitions.

There is a three-step analysis to determine if IRC §951B applies, and then (if it does), apply IRC §951B to other parts of the Internal Revenue Code to cause income inclusions.

Step 1. Normal Classification

Like all situations involving United States persons and foreign corporations, the first step is to do the normal analysis:

- Is this United States person a United States shareholder? IRC §951(b) applies, and downward attribution is prohibited by newly restored IRC §958(b)(4).

- Is this foreign corporation a CFC? Is more than 50 percent of its stock owned by United States shareholders? IRC §957 applies.

A “yes” answer to both will result in subpart F income inclusion (IRC §951(a)) and net CFC tested income inclusion (IRC §951A(a)).

Step 2. IRC §951B Classification

If you did not find United States shareholder and controlled foreign corporation status at Step 1, move on to Step 2 to re-analyze stock ownership using the special rules of IRC §951B(b) and (c):

- Is this United States person a foreign controlled United States shareholder? IRC §951B(b)(1) tells you how to figure that out.

- Is this foreign corporation a foreign controlled foreign corporation? IRC §951(c) tells you how to do this.

A foreign controlled United States shareholder is defined in IRC §951B(b):

For purposes of this section, the term “foreign controlled United States shareholder” means, with respect to any foreign corporation, any United States person which would be a United States shareholder with respect to such foreign corporation if:

(1) section 951(b) were applied by substituting “more than 50 percent” for “10 percent or more”, and

(2) section 958(b) were applied without regard to paragraph (4) thereof.

The job is simple: assume downward attribution applies (the effect of IRC §951B(b)(2)) and compute stock ownership. If the United States person owns more than 50 percent of the foreign corporation’s stock (IRC §951B(b)(1)), then you have a foreign controlled United States shareholder.

A foreign controlled foreign corporation is defined at IRC §951B(c):

For purposes of this section, the term “foreign controlled foreign corporation” means a foreign corporation, other than a controlled foreign corporation, which would be a controlled foreign corporation if section 957(a) were applied:

(1) by substituting “foreign controlled United States shareholders” for “United States shareholders”, and

(2) by substituting “section 958(b) (other than paragraph (4) thereof)” for “section 958(b)”.

Look at your foreign corporation. First, did you already decide that it is a controlled foreign corporation using the normal IRC §957(a) rules? If so, stop. The foreign corporation cannot be a foreign controlled foreign corporation. Second, rewrite IRC §957(a) to incorporate the changes required by IRC §951B(c)(1), (2):

For purposes of this title, the term “foreign controlled foreign corporation” means any foreign corporation if more than 50 percent of:

(1) the total combined voting power of all classes of stock of such corporation entitled to vote, or

(2) the total value of the stock of such corporation,

is owned (within the meaning of section 958(a)) or is considered as owned by applying the rules of ownership of section 958(b) (other than paragraph (4) thereof), byUnited States shareholdersforeign controlled United States shareholders on any day during the taxable year of such foreign corporation.

Third, determine whether foreign controlled United States shareholders own more than 50 percent of the foreign corporation’s stock using the stock ownership rules of IRC §958(a) and (b). When you apply the constructive ownership rules of IRC §958(b), calculate constructive ownership by including downward attribution (i.e., pretend that IRC §958(b)(4) does not exist).

Step 3. Income Inclusion Caused by Creative Rewriting

In Step 1, you determined United States shareholder and CFC status. Income inclusions are determined under IRC §951(a) and IRC §951A(a) in the usual fashion.

In Step 2, you again determined status—foreign controlled United States shareholder and foreign controlled foreign corporation status.

Here in Step 3, you apply IRC §951B(a) to cause a foreign controlled United States shareholder of a foreign controlled foreign corporation to have income inclusions under IRC §951(a) and IRC §951A(a) as if this were a United States shareholder of a controlled foreign corporation.

This is done through creative rewriting of the Internal Revenue Code.

How to Rewrite the Code When IRC §951B(a) Applies

If you have determined that you have a foreign controlled United States shareholder of a foreign controlled foreign corporation, IRC §951B(a) tells you what to do: rewrite almost all of subpart F (IRC sections 951–965) in specific ways.

No Rewrites for the Definitions of US Shareholder, CFCs

IRC §951B(a) does not apply to IRC sections 951(b) and 957. IRC §951B(a)(1).

The effect of this exclusion is to leave untouched the basic rules for determining whether a US person is a United States shareholder and whether a foreign corporation is a controlled foreign corporation. The Internal Revenue Code already knows how to tax a United States shareholder, so IRC §951B’s intervention is unnecessary.

Rewrites for Net CFC Tested Income

A foreign controlled United States shareholder of a foreign controlled foreign corporation includes net CFC tested income in that shareholder’s gross income.

IRC §951B(a)(2) says:

Section 951A (and such other provisions of this subpart as provided by the Secretary) shall be applied with respect to such shareholder:

(A) by treating each reference to “United States shareholder” in such section as including a reference to such shareholder, and

(B) by treating each reference to “controlled foreign corporation” in such section as including a reference to such foreign controlled foreign corporation.

“Such shareholder” means a foreign controlled United States shareholder of a foreign controlled foreign corporation.

Rewriting IRC §951A(a) to reflect IRC §951B(a)(2) (additions shown in bold):

Each person who is a United States shareholder or foreign controlled United States shareholder of any controlled foreign corporation or foreign controlled foreign corporation for any taxable year of such United States shareholder shall include in gross income such shareholder’s net CFC tested income for such taxable year.

Thus, IRC §951B(a) adds a new category of US taxpayers who have net CFC tested income inclusions: foreign controlled United States shareholders of foreign controlled foreign corporations.

Rewrite for Subpart F Income

A foreign controlled United States shareholder of a foreign controlled foreign corporation includes its pro rata share of subpart F income in its gross income by a simple game of word substitution. IRC 951B(a)(1) tells us to do Internal Revenue Code word games by substitution:

(a) In the case of any foreign controlled United States shareholder of a foreign controlled foreign corporation–

(1) this subpart (other than sections 951A, 951(b), and 957) shall be applied with respect to such shareholder (separately from, and in addition to, the application of this subpart without regard to this section)–

(A) by substituting “foreign controlled United States shareholder” for “United States shareholder” each place it appears therein, and

(B) by substituting “foreign controlled foreign corporation” for “controlled foreign corporation” each place it appears therein.

We must apply IRC §951B(a)(1) to IRC §951(a) because it is within “this subpart,” namely Subtitle A, Chapter 1, Subchapter N, Part III, Subpart F of the Internal Revenue Code (IRC sections 951–965), and it is not excluded by the parenthetical statement listing three provisions of subpart F for exclusion.

Applying IRC §951B(a)(1)’s instructions to rewrite IRC §951(a)(1)(A), we get:

If a foreign corporation is a

controlled foreign corporationforeign controlled foreign corporation at any time during any taxable year, every person who is aUnited States shareholder (as defined in subsection (b))foreign controlled United States shareholder of such corporation and who owns (within the meaning of section 958(a)) stock in such corporation on the last day, in such year, on which such corporation is acontrolled foreign corporationforeign controlled foreign corporation shall include in his gross income, for his taxable year in which or with which such taxable year of the corporation ends—

(A) his pro rata share (determined under paragraph (2)) of the corporation’s subpart F income for such year[.]

IRC §951B(a)(1) creates a ghost version of the IRC §951(a) subpart F income inclusion rule that applies the inclusion to a new category of United States persons: foreign controlled United States shareholder of foreign controlled foreign corporations.

Going back to the example, DomesticSub owns five percent of ForeignSub stock directly, as defined in IRC §958(a)(1)(A). IRC §951(a)(2) says to allocate ForeignSub’s subpart F income pro rata to a foreign controlled United States shareholder (because of IRC §951B) according to how much stock the foreign controlled United States shareholder owns directly or indirectly as defined in IRC §958(a).

Therefore, we have the unusual situation where a U.S. taxpayer with a tiny stock ownership percentage in a foreign corporation may (if the facts match the rules in IRC §951B) end up with income inclusion. A 10 percent or more direct or indirect stock ownership position is necessary for income inclusion for a United States shareholder, but ANY direct or indirect stock ownership is all it takes for income inclusion for a foreign controlled United States shareholder.

Other Sections in Subpart F

he same rule that we used for subpart F income inclusions (substitute “foreign controlled United States shareholder” for “United States shareholder,” and “foreign controlled foreign corporation” for “controlled foreign corporation”) will apply to all other provisions in subpart F. IRC §951B(a)(1).

For example, IRC §952(a) (the definition of subpart F income) will now begin:

For purposes of this subpart, the term “subpart F income” means, in the case of any

controlled foreign corporationforeign controlled foreign corporation, the sum of . . . .

Conclusion

For practitioners, here is some homework to do before new tax years start after Dec. 31, 2025:

- Revisit all holding structures and redetermine the status of United States shareholders and controlled foreign corporations. The restoration of IRC §958(b)(4) might mean fewer Form 5471 filing obligations.

- Look carefully at all holding structures that might be at risk of creating income inclusion for a domestic corporation because of IRC §951B and consider stock ownership changes to eliminate potential income inclusions on the domestic corporation’s tax return for upcoming years.