PFICs Inside SIPPs and Form 8621

Hello, it’s Phil Hodgen. Welcome to the Friday Edition, your every-other-week massive international tax missive.

New and Upcoming

- Free Webcast. Mark your calendars for this month’s International Tax Lunch session, which will be on March 27th at 9am Pacific Time. The topic is “Portfolio Interest Loans for Real Estate Investments,” hosted by yours truly. Stay subscribed for registration information.

- New Expatriation Video. Debra Rudd recorded a new video with guidelines on how to determine your expatriation date when you turn in your Form I-407. Find it here on our Youtube: What’s Your Expatriation Date?

- Debra Rudd Podcast Appearance. If you frequently work with green card holders, you may also enjoy Debra’s recent appearance on the Expat Wealth podcast. Debra and the host Richard Taylor dove into the short-term and long-term implications for giving up your green card.

- Hardcore AI for Tax Research. The International Tax Pros community is hosting one of its own for a one-hour presentation on using AI for tax research. Travis Call, CPA uses multiple AIs simultaneously to analyze tax issues and write up the conclusions. He will show you how he does it. Members attend free; just sign up inside the community. The nonmember price is $50; sign up here.

I get questions.

One of the recurring questions is about PFICs inside foreign retirement plans — like U.K. SIPPs:

Must the U.S. employee file Form 8621 for PFICs held inside the retirement plan?

Yes.

The High-Level Road Map

Assuming you have a trust (Reg. §301.7701-4(a)), you have to figure out how it and its participants are subject to U.S. income tax. There are only two categories of trusts:

- A trust where there is an “owner” of the trust. This is what we commonly call a grantor trust.

- All other trusts. This is what we commonly call a nongrantor trust (and you will find that phrase littered about in the Regulations), but we should more accurately call it a trust that does not have an owner, or just call it a trust.

When you have a grantor trust, IRC §671 says “make the owner pay the income tax on all of the trust’s income.”

When we see a trust that is not a grantor trust, we reflexively assume that IRC §§641-669 will apply to determine income tax results for the trust and its beneficiaries. This is where you find distributable net income, undistributed net income, etc. In fact, a trust and its beneficiaries can be taxed under one of two rulesets:

- IRC §§641-669.

- Not IRC §§641-669.

When would we NOT apply IRC §§641-669? Answer: when a regulation says so. Reg. §1.641(a)-0(a) says that if a trust is classified as an employees’ trust under IRC §402(b), then don’t apply Subchapter J at all.

Summarized succintly:

- There are only two categories of trusts: trusts that have owners, and trusts that don’t have owners.

- For trusts that don’t have owners, there are two ways to compute income tax liability:

- Subchapter J; or

- IRC §402(b).

When you look at it that way, you can see how we can distinguish reporting requirements from computation of income tax liability. Grantor trusts and nongrantor trusts have their own reporting requirements. Grantor trusts have one way that income tax liabilty is calculated and allocated between the trust and its owner. Nongrantor trusts have two ways in which the trust and its beneficiaries are taxed.

I’m going to show you that a SIPP is a nongrantor trust (for paperwork/filing purposes). It happens to be a nongrantor trust that computes its tax results under the employees’ trust rules of IRC §402(b). I’m going to show you that a SIPP cannot be a trust that has an owner. This conclusion drives the result that Form 8621 is required from a SIPP participant.

Let’s go. Paperwork and filing obligations, here we come.

Let’s Pretend

Let’s play pretend.

David is a U.S. citizen living in the United Kingdom. He owns 100% of the stock of a UK limited company that provides consulting services. David is the sole employee.

The company sets up a Self-Invested Personal Pension (SIPP) and makes employer contributions to it. The SIPP holds shares in a foreign mutual fund that qualifies as a PFIC. David is the sole beneficiary.

The question:

Must David file Form 8621 with respect to the PFIC shares held inside the SIPP?

Is the SIPP an “employees’ trust?”

Introduction

Before we can answer the Form 8621 question, we need to know what a SIPP is — for U.S. tax purposes. The type of entity will dictate the expected U.S. income tax treatment for the SIPP and the employee–David.

U.S. tax law doesn’t have an entity type called “retirement plan,” let alone “foreign retirement plan.” The Internal Revenue Code has qualified plans and nonqualified plans. Both types of plans hold their assets in trusts.

SIPPs hold their assets in trusts, too. How does the Internal Revenue Code classify the trust that holds a SIPP’s assets?

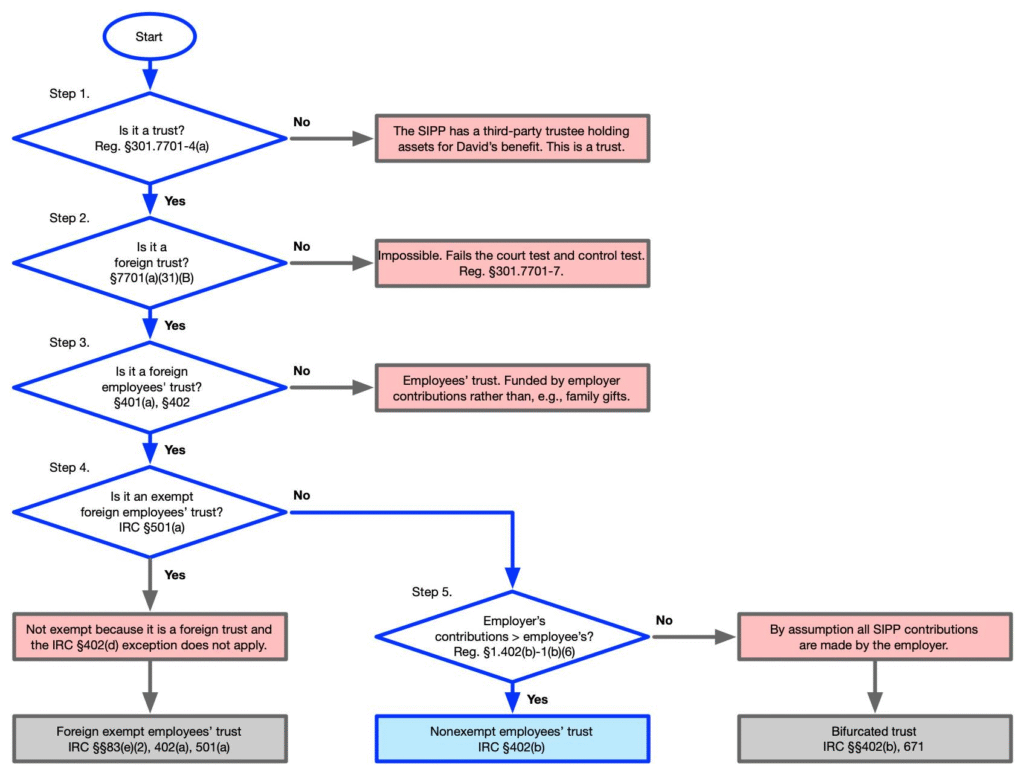

Flowchart

The flowchart below walks through the classification. The diamond shapes are questions that you answer either “yes” or “no.”

Step 1. Is it a trust?

Yes. The SIPP has a third-party trustee holding assets for David’s benefit and the trustee has fiduciary duties of care with respect to participants in the SIPP. Reg. §301.7701-4(a).

It is a trust.

Step 2. Is it a foreign trust?

Yes. A trust is “domestic” only if a U.S. court can exercise primary supervision over its administration and U.S. persons control all substantial decisions. Neither is true here, so the SIPP fails both tests. Reg. §301.7701-7.

It is a foreign trust.

Step 3. Is it a foreign employees’ trust?

Yes. A SIPP is a “pension plan” (created primarily for retirement benefits). David’s employer makes contributions to the SIPP for David’s benefit as an employee. The trust exists to fund retirement benefits earned through employment. It is not funded by family gifts or personal savings. IRC §§401(a), 402(a), (b).

It is a foreign employees’ trust.

Step 4. Is the foreign employees’ trust exempt from U.S. income tax under IRC §501(a)?

No. A trust is exempt under IRC §501(a) only if it is described in IRC §401(a). Exempt from income tax under IRC §501(a) just means that the trust does not pay income tax on its income from investments. To be exempt, the trust must satisfy a myriad of picky technical requirements in the Internal Revenue Code.

The SIPP was designed to satisfy U.K. legal and tax specifications, not to achieve U.S. tax exemption as a qualified plan. It cannot possibly satisfy all of the requirements of IRC §401(a). The one potential exemption will not apply. IRC §402(d) allows foreign retirement plans to be exempt plans for U.S. income tax purposes, but for reasons we don’t need to go into here, it will not apply to a SIPP.

The SIPP is not an exempt foreign employees’ trust.

Step 5. Is the trust bifurcated?

No. An employees’ trust will be treated partly as a foreign grantor trust if the employee’s contributions exceed the employer’s contributions. To make this explanation simple, I assumed that David’s employer makes all the contributions. There are no employee contributions to bifurcate.

Reg. §1.402(b)-1(b)(6) doesn’t split the trust into two pieces.

Conclusion

David’s SIPP is a nonexempt foreign employees’ trust. David’s U.S. income tax liability will be determined under IRC §402(b).

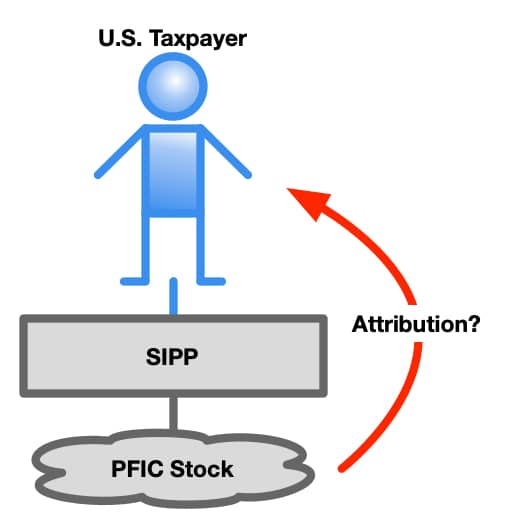

When is a SIPP Participant an Indirect Shareholder of a SIPP-Owned PFIC?

Remember–the SIPP is a trust without an owner. (A nongrantor trust to use imprecise language). With that in mind, let’s walk through the PFIC stock attribution rules. They have an attribution rule for exactly this kind of trust.

The pivotal question is “Will David be treated as the indirect owner of the SIPP-owned shares of PFIC stock?”

Attribution Rules for PFIC Stock Ownership

A PFIC is defined at IRC §1297(a). Let’s assume a PFIC exists.

A U.S. person who is a shareholder of a PFIC has a filing requirement. IRC §1298(f). A U.S. person is a shareholder of a PFIC by two different methods of stock ownership: direct ownership and indirect ownership. Reg. §1.1291-1(b)(7).

A U.S. person is an indirect shareholder in the PFIC stock attribution rules described in Reg. §1.1291-1(b)(8). Indirect stock ownership through a grantor trust is defined in Reg. §1.1291-1(b)(8)(iii)(D). Indirect PFIC stock ownership through a nongrantor trust is defined in Reg. §1.1291-1(b)(8)(iii)(C).

The Grantor Trust Attribution Rule Does Not Apply to a SIPP

Let’s get rid of the easy one first. The attribution rules for PFIC stock ownership through a grantor trust will not apply to a SIPP.

Reg. 1.1291-1(b)(8)(iii)(D) Grantor trusts. If a foreign or domestic trust directly or indirectly owns stock, a person that is treated under sections 671 through 679 as the owner of any portion of the trust that holds an interest in the stock is considered to own the interest in the stock held by that portion of the trust.

David, our U.S. citizen employee/participant in a U.K. SIPP, is not a person “treated under sections 671 through 679 as the owner of . . . the trust.”

- IRC §671 is the general rule describing an owner’s tax treatment. IRC §672 contains definitions. Neither section makes David an owner.

- He cannot be the owner of the trust under IRC §§673-677 because these rules require the individual to be a “grantor” and also to have made a gratuitous transfer to the trust. Reg. §1.671-2(e)(1). David did not make a transfer to the SIPP at all–the employer made the transfer.

- He cannot be the owner of the trust under IRC §678 because he does not have the required power to force distributions to himself at any time. The trustee stands in the way.

- He cannot be the owner of the trust under IRC §679 because this section requires a U.S. transferor to a foreign trust to be the owner of that trust. The transferor is the employer, a foreign corporation.

Conclusion: David is not the owner of the SIPP under the grantor trust rules, so the PFIC stock attribution rules of Reg. §1.1291-1(b)(8)(iii)(D) do not apply.

The Trust-Without-an-Owner Attribution Rule Applies to a SIPP

The Rule

The PFIC stock attribution rule attributes stock ownership to beneficiaries of trusts that do not have owners. The Regulations use the phrase “nongrantor trust” to describe these trusts:

Reg. 1.1291-1(b)(8)(iii)(C) Estates and nongrantor trusts. If a foreign or domestic estate or nongrantor trust (other than an employees’ trust described in section 401(a) that is exempt from tax under section 501(a)) directly or indirectly owns stock, each beneficiary of the estate or trust is considered to own a proportionate amount of such stock. For purposes of this paragraph (b)(8)(iii)(C), a nongrantor trust is any trust or portion of a trust that is not treated as owned by one or more persons under sections 671 through 679.

The SIPP is a “Nongrantor” Trust

There is a definition of nongrantor trust–a trust without an owner. Reg. 1.1291-1(b)(8)(iii)(C) says:

For purposes of this paragraph (b)(8)(iii)(C), a nongrantor trust is any trust or portion of a trust that is not treated as owned by one or more persons under sections 671 through 679.

If a trust is not owned by a person under IRC §§671-679, then the trust is a nongrantor trust. This demonstrates the binary view of trusts that I outlined above: for purposes of PFIC stock attribution, trusts come in exactly two flavors. To get Biblical, there are only sheep and goats.

As demonstrated above, David is not the owner of the SIPP under IRC §§671-679. The employer is not the owner of the SIPP for purposes of IRC §671, either. One reason is that the employer’s contribution to the trust is not gratuitous–it’s a payment for services rendered.

Therefore, for the purposes of the PFIC stock attribution rule, the SIPP is a nongrantor trust.

Therefore, David is an Indirect PFIC Shareholder

Now that we have decided that the SIPP is a nongrantor trust for purposes of the PFIC stock attribution rules, we can go back and apply the attribution rule of Reg. §1.1291-1(b)(8)(iii)(C).

If a foreign or domestic estate or nongrantor trust (other than an employees’ trust described in section 401(a) that is exempt from tax under section 501(a)) directly or indirectly owns stock, each beneficiary of the estate or trust is considered to own a proportionate amount of such stock.

The SIPP, we decided for the purposes of Reg. §1.1291-1(b)(8)(iii)(C), is a nongrantor trust. It directly owns PFIC stock. Therefore each beneficiary owns a proportionate amount of the PFIC stock. David is the only beneficiary, so he owns 100% of the PFIC stock.

The SIPP is not an Exempt Trust

The attribution rule does not treat a beneficiary of an employees’ trust under IRC §401(a) as the indirect shareholder of trust-owned PFIC stock.

Do not let your heart leap with eager anticipation at the sight of the words “employees’ trust.” The exception is not for the kind of employees’ trust that the SIPP happens to be. Reg. §1.1291-1(b)(8)(iii)(C) says (emphasis added):

If a foreign or domestic estate or nongrantor trust (other than an employees’ trust described in section 401(a) that is exempt from tax under section 501(a)) directly or indirectly owns stock, each beneficiary of the estate or trust is considered to own a proportionate amount of such stock.

A SIPP is an employees’ trust, but it is NOT an employees’ trust that is exempt from tax under IRC §501(a). Therefore, the exception will not apply to the SIPP, and the default rule attributing PFIC stock ownership to the beneficiary–David, the employee–will remain intact.

Conclusion: Filing Requirement

David, an (indirect) shareholder of PFIC stock, will have a Form 8621 filing requirement for all of the PFIC stock held in the SIPP.

The IRC §401(a) carveout tells us something about the drafter’s intent. Treasury knew that employees’ trusts would be covered by this attribution rule. It carved out qualified plans–exempt trusts. It did not carve out nonexempt employees’ trusts–like the SIPP. That omission reinforces the conclusion that a nonexempt employees’ trust remains within the rule.

Even if you have a filing requirement, an exception might save you. Look at the Instructions for Form 8621 for details, but the most likely interesting filing exception is the treaty exception. See Reg. §1.1298-1(c)(4).

What Next?

First, do not panic. There is no penalty for failure to file Form 8621. The only downside is “the statute of limitations on everything is open forever” problem created by IRC §6501(c)(8).

Second, notice that I have studiously avoided talking about the impact of PFICs owned by SIPPs on the taxable income of the employee. Will excess distributions from the PFIC bleed upstream through the SIPP to the employees’ income tax return? I will write about that next time. Wait before you make a decision on what to do.